Much of the conversation around tokenization has focused on gold and, to a lesser extent, silver. That makes sense—both are stores of value, widely recognized, and relatively standardized.

But a quieter shift is now underway.

Industrial metals are beginning to enter the blockchain conversation.

Unlike precious metals, industrial metals—such as copper, aluminum, and nickel—are not stores of value. They are inputs to the real economy, essential to infrastructure, energy systems, and manufacturing.

So why tokenization?

The answer lies in three areas:

Supply chain complexity

Demand for transparency and provenance

The ongoing financialization of commodities

Tokenization offers the potential to improve tracking, reduce settlement friction, and enhance visibility across fragmented global supply chains.

But challenges remain.

Industrial metals lack the standardization of gold. They vary by grade, form, and end use. That makes token design—and trust—more difficult.

Not all metals are equally viable. Copper and aluminum may be strong candidates. Raw ore and specialized alloys, far less so.

So is this the next frontier—or premature?

Likely both.

Tokenization of industrial metals is not about creating digital money—it is about modernizing the infrastructure of the real economy.

Why Junior Mining Boards Must Balance Accountability with Executive Leadership

Leadership in junior mining companies is often highly concentrated. In many small mining companies, the Chief Executive Officer (CEO) is responsible for corporate leadership, raising capital, guiding exploration strategy, managing investor relations, and coordinating technical teams. That’s a heavy load. He (occasionally she, but for the purpose of this article, let’s say he) must do it all.

That reality raises an important governance question: How should the board of directors oversee the CEO without undermining his ability to lead? Too little oversight creates risk. Too much oversight creates paralysis. The challenge for boards—particularly in junior mining companies—is finding the balance between accountability and trust. In other words, the Goldilocks spot. Let’s explore that issue today.

The Unique Governance Environment of Junior Mining

Unlike large operating mining companies, junior mining firms typically operate with very lean management teams. Lean being the operative word. The CEO often wears multiple hats: strategist, fundraiser, spokesperson, and operational coordinator. At the same time, the company is spending investor capital long before revenue exists. That reality makes oversight essential.

Keep this point in mind: shareholders invest in junior mining companies largely based on two factors:

The quality of the geological opportunity.

The credibility of the management team.

The CEO sits at the center of both. Hence, boards must ensure that the CEO is operating effectively, ethically, and in alignment with shareholder interests. But oversight must be exercised in a way that supports leadership rather than interfering with it.

The Board’s Role: Oversight, Not Operations

A common governance mistake in early-stage companies occurs when directors drift into operational management. This mistake is often made without intent or malice. Nevertheless, it happens. Board members may have deep technical expertise, decades of industry experience, or prior involvement with similar projects. When challenges arise—as they inevitably do in mining—the temptation to intervene directly can be strong. However, boards do not run companies. Management does.

The board’s responsibility is to provide oversight, guidance, and accountability—not to manage daily operations. In practical terms, effective boards focus on questions such as:

Is the CEO executing the company’s strategy effectively?

Are investor funds being deployed responsibly?

Are risks being identified and managed appropriately?

Is communication with shareholders transparent and credible?

These questions represent governance oversight—not operational control.

Setting Clear Expectations

One of the most effective ways boards can oversee the CEO without micromanaging is by adopting a clear mission statement, governance protocols, and establishing clear expectations from the outset. For example, the board may adopt a formal resolution that includes, but is not limited to:

Strategic objectives for the company

Performance expectations for management

Capital allocation priorities

Reporting standards for the board

Instead of directors debating individual operational decisions, they can evaluate whether management’s actions align with agreed-upon strategic goals. When expectations are clearly defined, oversight becomes far more constructive. This approach strengthens accountability while preserving management’s ability to execute.

Performance Evaluation

Oversight of the CEO must ultimately include some form of performance evaluation. Please note, there is no need for rigid bureaucracy. However, the board should periodically assess whether the CEO is meeting the company’s strategic and operational objectives. This can be an agenda item during quarterly board meetings, for instance. Key areas of evaluation should include:

Advancement of exploration programs

Effectiveness in raising capital

Quality of investor communications

Team leadership and organizational development

Adherence to governance and reporting standards

Items three and four are more challenging to evaluate; therefore creativity may be required. Nevertheless, these evaluations provide an opportunity for constructive feedback and ensure that the board remains engaged in its oversight responsibilities.

Supporting the CEO

Oversight should not be confused with opposition. Strong boards do not exist to second-guess management at every turn. Boards serve as strategic partners who help leadership navigate complex decisions. That’s a big difference.

Junior mining companies operate in a high-risk environment. Results are uncertain. Financing conditions can change quickly. Commodity markets fluctuate. During these periods, a thoughtful board can provide valuable perspective to the CEO. Experienced directors may help management evaluate strategic alternatives, assess risk, or think through financing strategies. This type of support strengthens leadership rather than weakening it.

The Importance of Independent Directors

Independent directors possess a special authority—independence. They are not part of the inner network circle. In fact, they are chosen precisely because they bring an independent voice to the boardroom. Their outsider status means they are well suited to evaluate management performance objectively. Moreover, they serve as an important governance safeguard when difficult decisions arise. Consider the following situations where independent directors are particularly important:

CEO compensation decisions

Performance evaluations

Conflict-of-interest oversight

Major strategic transactions

Audit committee leadership

By placing these responsibilities in the hands of independent directors, boards can maintain appropriate oversight while avoiding operational interference. Let’s now turn to the micromanagement trap that directors often fall into.

Avoiding the Trap of Micromanagement

Micromanagement is one of the most common governance pitfalls in smaller companies. It often begins with good intentions. I have personally witnessed this situation. Here is why it happens.

Directors want to help. They want to apply their experience. They want to protect shareholder interests. But when board members begin directing operational decisions—approving minor expenditures, managing staff interactions, or influencing day-to-day activities—the governance structure breaks down. Management becomes hesitant. Decision-making slows. Accountability becomes blurred. In short, micromanagement weakens both the board and the CEO.

Governance as Leadership Discipline

The best junior mining companies understand that governance is not simply a compliance exercise. It is a leadership discipline. Effective boards hold CEOs accountable while also empowering them to lead. They set strategic direction without interfering with execution. They ask difficult questions without undermining management authority. Most importantly, they remain focused on the make-or-break decisions that protect the long-term interests of shareholders.

Final Thoughts

Junior mining companies operate in a challenging environment. There is no way to sugarcoat that reality. Exploration risk is high, capital is precious, and management teams are often small. Under these conditions, the relationship between the board and the CEO becomes critically important.

Too little oversight can expose investors to unnecessary risk. Too much oversight can suffocate leadership. The most effective boards understand that their role is not to manage the company—but to ensure that it is well led. That balance requires discipline.

And like all aspects of governance before revenue, discipline is what ultimately builds credibility with investors and strength within the organization.

Are Industrial Metals Ready to Join the Blockchain World

The conversation around tokenization has, to date, been dominated by precious metals—particularly gold and, to a lesser extent, silver. That focus has been logical. Gold is a store of value, widely recognized, and relatively standardized. Silver, too, has been a store of value for thousands of years and remains so in many parts of the world. Hence, both lend themselves naturally to tokenization. But a quieter shift is now beginning to take shape.

Industrial metals—long defined by their role in production rather than wealth preservation—are starting to enter the blockchain conversation. This development raises an important question: can metals defined by utility, variability, and complex supply chains be effectively tokenized? Or does their very nature resist the structure required for digital representation? Read along to find out, but first we start with a definition: what are industrial metals?

What Are “Industrial Metals”?

Industrial metals are those primarily used in manufacturing, construction, and technology rather than as stores of value, a unit of account, or a medium of exchange. In other words, industrial metals are not money nor currency. While industrial metals don’t function as money, they are the backbone of the real economy. No industrial metals equals no modern society. Consider these common examples:

• Copper Aluminum

• Nickel Zinc

• Lead Tin

What do they all have in common? These metals are essential inputs for:

• Infrastructure and construction

• Energy systems (including renewables)

• Electronics and manufacturing

• Transportation and industrial machinery

Unlike gold or silver, their value is not driven by monetary psychology; it is driven by economic activity and industrial demand.

Why Industrial Metals Are Now Entering the Tokenization Conversation

Three structural shifts are driving interest in tokenizing industrial metals. Let’s examine each one below.

1. Supply Chain Complexity

Industrial metals move through long, fragmented supply chains:

• Extraction

• Refining

• Transportation

• Storage

• Delivery

Each stage introduces friction, opacity, and inefficiency. Tokenization offers the potential to:

• Track ownership more precisely

• Improve transparency

• Reduce settlement delays

In theory, a token could represent a specific quantity of metal at a defined point in the supply chain—creating a more efficient system of transfer and verification. Now, point two.

2. Demand for Transparency and Provenance

As global supply chains come under scrutiny—particularly around environmental and geopolitical issues—there is growing demand for:

• Verified sourcing

• ESG compliance

• Chain-of-custody tracking

Blockchain infrastructure is well-suited to this challenge. Tokenized metals are capable of:

• Recording origin

• Tracking movement

• Providing immutable audit trails

This is particularly relevant for metals used in:

• Electric vehicles

• Renewable energy systems

• Advanced manufacturing

3. Financialization of Commodities

Industrial metals are already heavily traded. Traders often use:

• Spot markets

• Futures contracts

• Exchange-traded products

Tokenization represents a potential next step in the technological evolution—bringing:

• Faster settlement

• Fractional access

• New liquidity channels

However, unlike gold, industrial metals are not typically held for investment. That distinction matters.

How Industrial Metals Might Be Tokenized

We now turn to the “how” in the process. The tokenization of industrial metals can take several forms, each with different implications. Let’s walk through the possibilities.

1. Warehouse-Backed Tokens

The most straightforward model mirrors tokenized gold:

• A token represents a specific quantity of metal

• Stored in a certified warehouse

• Backed by documented inventory

This approach works best when:

• The metal is standardized

• Storage conditions are stable

• Inventory is clearly defined

2. Supply Chain Tokens

A more complex model involves tokenizing metals in motion. This model is much more ambitious—not impossible, just more difficult. If successful, it might look like this:

• Representing metal at various stages (ore, refined, shipped)

• Linking tokens to logistics data

• Updating ownership as the metal moves

3. Production-Linked Tokens

In some cases, tokens could represent:

• Future production

• Offtake agreements

• Rights to delivery

This begins to blur the line between commodities and financial contracts. This, of course, introduces additional layers of risk—a field day for securities lawyers.

Which Industrial Metals Are Strong Candidates?

Not all industrial metals are equally suited for tokenization. Below, they are divided into most viable, moderately viable, and less viable categories based on market structure, standardization, and practical considerations.

Most Viable Candidates

Copper

• Highly standardized

• Globally traded

• Critical for electrification and energy systems

Strong candidate due to liquidity and uniformity

Aluminum

• Widely used

• Standardized forms (ingots, billets)

• Established global markets

Suitable for warehouse-backed token models

Nickel

• Increasing demand (EV batteries)

• Growing interest in supply chain transparency

Viable, particularly with ESG tracking

Moderately Viable

Zinc and Tin

• Smaller markets

• Less investor attention

• Still standardized

Possible, but with limited initial demand

Which Metals Are Less Viable—and Why

Lead

• Declining industrial relevance

• Environmental concerns

Limited investor and institutional interest

Highly Specialized Alloys

• Non-standardized

• Variable composition

• Difficult to verify consistently

Poor candidates for tokenization

Raw Ore

• Highly variable

• Quality differences

• Requires processing

Not suitable for direct token representation

The Core Challenge: Standardization vs. Reality

The central issue with industrial metals is not technology—it is standardization. Without standardization, it becomes an uphill climb.

Gold works because:

• One ounce is interchangeable with another

• Quality is universally defined

Industrial metals, by contrast:

• Vary by grade

• Differ by form

• Depend on end-use requirements

This creates friction in token design. While tokens can be non-fungible (NFTs), that only adds complexity.

For tokenization to work, the system must answer:

• What exactly does the token represent?

• Where is the metal located?

• What are its specifications?

Without clear answers, the token risks becoming:

• Ambiguous

• Illiquid

• Distrusted

Governance Still Matters

As with precious metals, tokenization does not eliminate the need for governance—it amplifies it.

Key considerations include:

• Custody and storage verification

• Audit frequency and transparency

• Legal ownership rights

• Redemption mechanisms

In industrial metals, these issues are even more complex due to:

• Supply chain variability

• Multiple stakeholders

• Jurisdictional differences

Without strong governance frameworks, tokenized industrial metals risk becoming:

• Conceptually appealing

• Practically unreliable

So—Is This a Real Shift or Premature?

Industrial metals are unlikely to follow the same path as gold or silver. They are not primarily:

• Stores of value

• Monetary hedges

They are:

• Inputs

• Tools

• Economic enablers

That distinction means tokenization will likely develop differently. Instead of focusing on investment demand, the more appropriate focus may be efficiency, transparency, and logistics applications.

Final Thoughts

Industrial metals are beginning their blockchain moment—but it will not look like gold’s. This is not about creating digital stores of value. It is about modernizing the infrastructure that supports the real economy using blockchain technology.

The opportunity is significant:

• More transparent supply chains

• Faster and more efficient transactions

• Improved verification and trust

But the challenges are equally real:

• Lack of standardization

• Complex logistics

• Greater governance requirements

As with any emerging system, the outcome will depend not on the technology itself, but on how it is implemented. Tokenization can bring structure to complexity—but only if the underlying system is clearly defined and rigorously governed. In the case of industrial metals, that work is just beginning.

Why Junior Mining Companies Must Manage Conflicts of Interest with Transparency and Structure

The junior mining industry is built on relationships; is that a blessing or a curse? It all depends. Geologists, financiers, promoters, engineers, and investors often work together across multiple ventures over the course of their careers. It’s not unusual for yesterday’s successful exploration team to reunite to create tomorrow’s even bigger hit! Therefore, the challenge is not the existence of these relationships. The challenge is managing them with discipline.

In the mining sector, an interconnected ecosystem is generally a strength. Experience travels with people, and seasoned professionals often bring trusted partners with them when launching new ventures. For early-stage mining companies, those relationships can accelerate exploration programs, attract capital, and help advance projects efficiently. Unfortunately, the same relationships that make the industry effective can also introduce governance risks today and beyond.

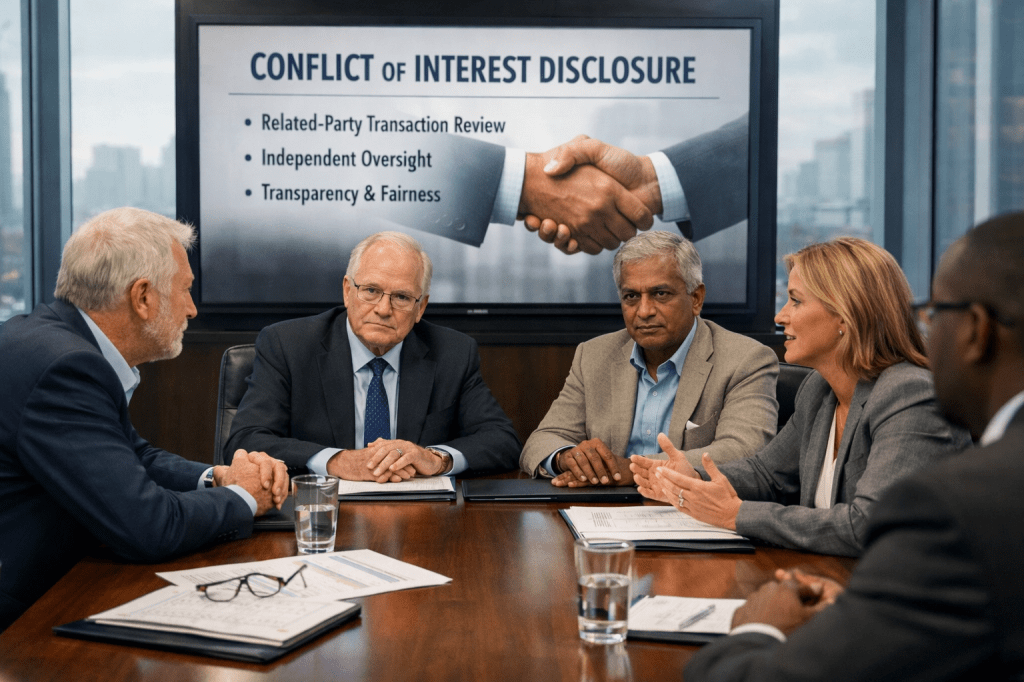

For junior mining companies seeking credibility in capital markets, the careful oversight of related-party transactions is essential. Investors must be confident that decisions involving insiders are evaluated objectively and that the interests of the company—and its shareholders—come first. When directors, officers, or major shareholders conduct business with the company itself, the transaction becomes what regulators and investors refer to as a related-party transaction. These arrangements are common in junior mining companies and are not inherently improper. When managed properly, such arrangements may be legitimate and even beneficial to the company. When poorly governed, they undermine investor trust, damage corporate credibility, and create regulatory scrutiny. For junior mining companies operating in the exploration and development stages, disciplined oversight of related-party transactions is not optional. It is an essential element of responsible governance.

Independent board oversight ensures related-party transactions are evaluated objectively for shareholders' best interests.

Understanding Related-Party Transactions

A related-party transaction occurs when a company conducts business with individuals or entities that have a close relationship with the organization. These relationships can include directors, officers, major shareholders, or businesses controlled by them.

Examples commonly seen in junior mining companies include:

Consulting agreements with directors or executives

Technical services provided by companies owned by insiders

Office leases involving board members or founders

Financing arrangements with major shareholders

Equipment or service contracts with affiliated firms

These transactions are not inherently improper. For some investors, these transactions could signal a positive indicator because it may mean insiders believe in the company. But as noted twice, it all depends. The governance challenge lies not in avoiding these transactions entirely, but in ensuring that they are conducted transparently, fairly, and in the best interests of the company.

The Importance of Conflict Discipline

Effective governance requires conflict-of-interest discipline. This means recognizing when personal interests intersect with corporate decision-making and establishing procedures that prioritize the company’s integrity rather than personal interests. Conflict discipline is focused on four considerations:

Decisions are made in the best interests of the company

Financial terms are fair and reasonable

Independent oversight is applied where appropriate

Investors receive transparent disclosure

Without these safeguards, related-party transactions can create the perception—whether accurate or not—that insiders are benefiting at the expense of shareholders. In capital markets, perception matters—a lot. Investors evaluating junior mining companies are not only assessing geology and project potential. They are also evaluating governance quality. Weak conflict management can raise concerns about transparency and accountability, ultimately affecting investor confidence.

The Role of Independent Directors

Why and how do independent directors play a critical role in reviewing and approving related-party transactions? First, they are not directly involved in management or financially tied to the proposed transaction. Their independence translates into being better positioned to evaluate whether a particular arrangement is fair to the company. Emphasis added—the company.

Typical governance practices include:

Requiring full disclosure of potential conflicts

Recusal of interested directors from decision-making

Independent review by the board or a committee

Documentation of the evaluation process

Companies that adopt best practices often empower the audit committee or a special committee of independent directors to review and approve related-party transactions before full board action. This process protects both the company and the individuals involved. It ensures that decisions are evaluated objectively and that governance standards remain intact.

Transparency and Disclosure

As sunshine is a great disinfectant, transparency is one of the most effective safeguards in managing conflicts of interest. Public mining companies are typically required to disclose related-party transactions in their financial statements and regulatory filings. Private companies should do so as well. These disclosures allow investors to understand the nature of the transaction and evaluate whether appropriate governance procedures were followed.

Clear disclosure generally includes:

The parties involved in the transaction

The financial terms of the arrangement

The nature of the relationship

The governance process used to approve the transaction

When companies provide clear and transparent disclosure, investors are better able to evaluate the transaction on its merits. Opacity, on the other hand, often raises more concerns than the transaction itself.

Protecting Investor Confidence

Junior mining companies, by definition, depend heavily on investor capital to finance exploration programs and project development. As a rule, exploration companies operate without revenue for extended periods; thus investor trust becomes one of the company’s most valuable assets. Lose it; lose investors.

Strong governance practices—including disciplined oversight of related-party transactions—help protect that trust. Investors are far more comfortable supporting companies that demonstrate:

Clear governance policies

Independent board oversight

Transparent disclosure practices

Documented decision-making processes

These practices signal that the company is committed to protecting shareholder interests.

Establishing Clear Policies Early

Many governance challenges in junior mining companies arise not from bad intentions but from the absence of clear procedures. However, good intentions are not sufficient when it comes to capital. Establishing formal policies early in the life of the company is what counts and can prevent confusion and reduce governance risks.

Effective related-party transaction policies typically include:

Formal disclosure requirements for directors and officers

Independent review of potential conflicts

Recusal procedures for interested parties

Board documentation of transaction approvals

These policies do not prevent companies from working with experienced insiders or affiliated firms. Instead, they provide a structured framework for evaluating such relationships responsibly. In other words, the objective is not to eliminate relationships—it is to govern them properly.

Governance as a Signal to the Market

In the competitive world of junior mining, governance quality increasingly influences how investors, partners, and strategic acquirers evaluate companies. Moreover, initial quality capital often attracts even stronger investors. Strong conflict management practices send a clear signal to the market: the company understands the importance of transparency, fairness, and disciplined decision-making.

That signal can strengthen investor confidence, reduce perceived governance risk, and ultimately support capital formation. Conversely, poorly managed related-party transactions can create lasting reputational damage that is difficult to repair.

Final Thoughts

Relationships are common in the junior mining sector. Industry participants often collaborate across multiple projects and companies over many years. These relationships can bring valuable expertise and capital to early-stage mining ventures. However, these relationships must be managed with care lest they become a hindrance.

Related-party transactions require clear disclosure, independent oversight, and disciplined governance processes. When handled properly, they can support the growth of a company while maintaining investor trust. When handled poorly, they can erode the very confidence that junior mining companies depend upon.

Governance before revenue is ultimately about stewardship. Stewardship begins with the discipline to manage conflicts of interest with transparency and integrity.

When geopolitical tensions rise, markets respond quickly—and often predictably. The recent escalation of conflict involving Iran and the resulting spike in oil prices have once again pushed inflation concerns back to the forefront. Energy costs ripple through the global economy, raising transportation, production, and ultimately consumer prices. This is where we find ourselves now. That’s why its no surprise that in moments like these, investors instinctively return to a familiar question:

Where can capital go to preserve value when inflation accelerates?

For centuries, the answer has often been precious metals, particularly gold. But in 2026, a new variation of that question is emerging: do tokenized precious metals offer the same protection—or are they simply a digital wrapper around an old idea?

Inflation, Uncertainty, and the Return of Hard Assets

Inflation is not merely a number—it is a psychological force. I say psychological force based on my recent trip through Argentina; a nation where inflation was running at 200% just a few years ago. The people who I interacted with were definitely impacted psychologically–they don’t believe in fiat.

When prices begin to rise, confidence in fiat currency weakens, and investors look for assets that are:

Scarce

Tangible

Globally recognized

Gold has historically met all three criteria. Silver, to a lesser extent, has followed a similar path. These metals are not tied to any single government or monetary policy, making them attractive during periods of uncertainty. Neither gold or silver is subject to counter-party risk if they are in your possession.

The current environment—marked by geopolitical tension, energy price volatility, and shifting monetary expectations—has once again highlighted the role of hard assets as a defensive allocation. But traditional ownership of precious metals comes with friction:

Storage costs

Limited liquidity

Physical transfer challenges

This is where tokenization enters the conversation.

What Tokenized Precious Metals Actually Represent

At their core, tokenized precious metals are digital tokens issued on a blockchain that represent ownership of physical metal held in custody. When properly executed, each token corresponds to:

A specific quantity of metal (e.g., one troy ounce of gold)

Stored in a professional vault

Backed by audited reserves

This is no longer theoretical. Well-known examples include:

Paxos Gold (PAXG)

Tether Gold (XAUT)

Kinesis (KAU/KAG)

The promise is straightforward: Combine the stability of physical metals with the efficiency of digital assets. Investors can:

Buy fractional amounts

Transfer instantly

Trade globally

Potentially redeem for physical metal

On paper, this appears to solve many of the traditional limitations of owning gold or silver. But the key question remains: Does tokenization enhance, dilute, or have no impact on the inflation-hedging properties of metals?

The Case FOR Tokenized Metals as an Inflation Hedge

1. Direct Exposure to Physical Assets

Unlike mining stocks or derivatives, tokenized metals are designed to represent direct ownership of underlying bullion. During inflationary periods, investors are not seeking leverage or speculation—they are seeking preservation of capital and their purchasing power. Tokenized metals, when properly structured, maintain this direct linkage.

2. Improved Liquidity and Accessibility

Traditional gold ownership can be cumbersome. Tokenization lowers barriers by allowing:

Fractional ownership

24/7 trading

Global access

This expands participation and allows more investors to allocate to hard assets quickly—particularly during fast-moving macro events like energy-driven inflation spikes. The more gold is used as a store of value versus fiat currency, whether physical or tokenized, gold holders are better off.

3. Faster Settlement in Uncertain Markets

In times of crisis, liquidity matters as much as asset quality. This is where tokenized gold “shines”; no pun intended. Tokenized metals can settle transactions in minutes, or even seconds, rather than days, offering:

Greater flexibility

Faster reallocation of capital

This is especially relevant in volatile environments where timing becomes critical. Just think about trying to leave Dubai, for instance, with physical gold on an airplane during these moments.

4. Integration with Digital Financial Systems

As financial systems evolve, tokenized assets are increasingly positioned to interact with:

Digital wallets

Decentralized finance platforms

Cross-border payment systems

This may enhance their utility compared to traditional bullion, particularly in a world where financial infrastructure is becoming more digitized. Consider this question: is there any good reason why gold holders should function with 2026 BC technology? I say no. I say 2026 AD technology should be the way.

The Case AGAINST: Where the Risks and “Hype” Begin

While the advantages are real, tokenized metals introduce a new layer of risk that investors must understand. Should this be a surprise? Of course not. Nothing is risk free in life. Hence, let’s examine the case against tokenized gold and silver.

1. Counterparty and Custody Risk

Unlike holding physical gold directly, tokenized metals rely on a chain of trust:

Issuer

Custodian

Auditor

If any link in that chain fails, the integrity of the token is compromised. Therefore, investors should ask, at a minimum:

Is the metal allocated and segregated?

Are bar lists publicly available?

How frequently are audits conducted—and by whom?

Without clear answers, the “token” may be more symbolic than secure.

2. Redemption Practicality

Many tokenized metals advertise physical redemption, but the reality can be more complex:

Minimum redemption thresholds

Fees and logistics

Geographic limitations

If redemption is impractical for most holders, the token behaves less like physical ownership and more like a synthetic instrument. Check into these consideration before, much before, spending a dollar on tokenized gold or silver.

3. Regulatory Ambiguity

Tokenized metals exist at the intersection of commodities, securities, and digital assets. Regulatory frameworks are still evolving.

This creates uncertainty around:

Investor protections

Legal recourse

Jurisdictional oversight

In times of market stress, these uncertainties can become more pronounced.

4. Market Perception Risk

An inflation hedge must not only function—it must be trusted. Gold’s value is reinforced by centuries of acceptance. Tokenized metals, by contrast, are still establishing credibility. With time, the younger generation will consider tokenized gold and silver as natural. They may even ask, why all the fuss in 2026. However, during this period of transition perception risk is a factor in the market among the boomer generation. If confidence in a specific issuer weakens, the token’s price may diverge from the underlying metal—undermining its role as a hedge.

Tokenized Metals vs Traditional Alternatives

To understand whether tokenized metals are a true hedge, they must be compared to existing options:

Physical Bullion

Highest level of control

Lowest counterparty risk

Lowest liquidity

Gold ETFs

Highly liquid

Easy to trade

Indirect ownership (no redemption for most investors)

Futures Contracts

Leverage available

Complex and time-sensitive

Not designed for long-term holding

Tokenized Metals

Direct (but mediated) ownership

High liquidity

Dependent on issuer structure and trust

So—Hedge or Hype?

The answer is not binary. Tokenized precious metals are not hype in the sense that they represent a real and meaningful innovation. They address genuine inefficiencies in how physical metals are owned and traded. However, they are also not a perfect substitute for traditional safe-haven assets yet. On the way; not there yet.

Essentially, their effectiveness as an inflation hedge depends on one critical factor: The strength and transparency of the underlying structure. When properly designed—with:

Allocated, audited reserves

Clear redemption mechanisms

Credible custodians

—they can function as a legitimate extension of physical metals into the digital age.

When poorly structured, they risk becoming:

Opaque

Illiquid in practice

Dependent on trust rather than verification

Final Thoughts

The current geopolitical environment serves as a reminder that inflation is not an abstract concept—it is a lived reality driven by events, policy, and market psychology. As oil prices rise and uncertainty spreads, the search for stability intensifies.

Tokenized precious metals sit at an interesting intersection:

Old-world value (gold and silver)

New-world infrastructure (blockchain)

They are not a replacement for traditional hedges—but they are an evolution. For investors willing to do the work—examining custody, auditing, and redemption—tokenized metals can play a role in a modern portfolio. Discipline matters in every system of governance system and market structure.

Not all tokens are created equal. And in inflationary environments, the difference between structure and assumption can determine whether an asset protects value—or merely promises to.