by Yogi Nelson (Nelson Hernandez)

Tokenization, the Promise and the Gap

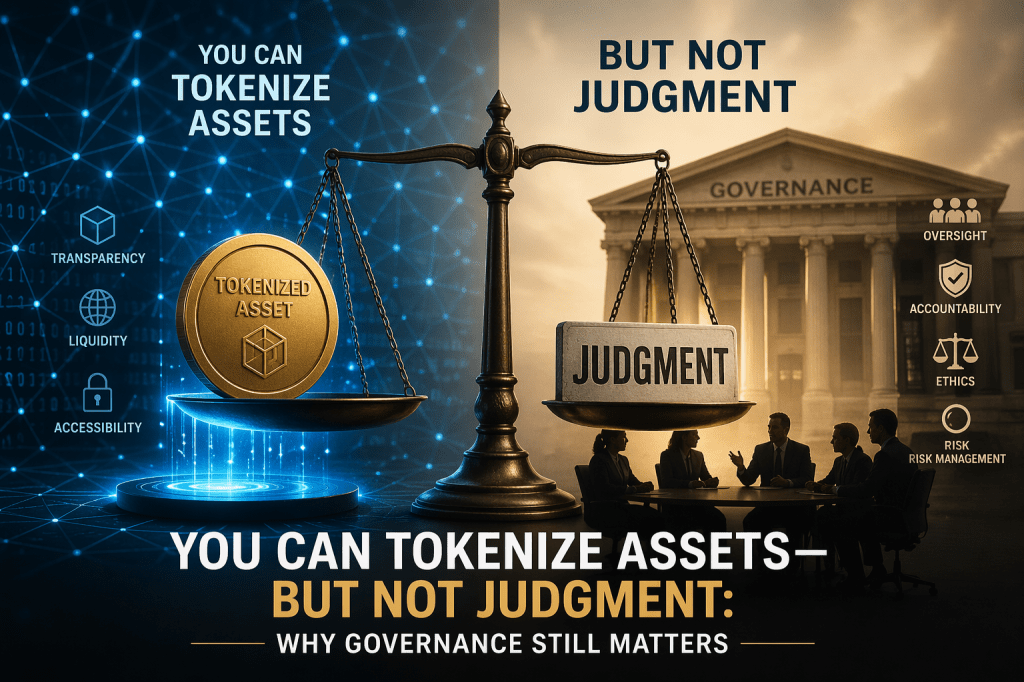

Can assets be tokenize? Absolutely yes. The more important question is, can judgement be tokenize? Absolutely not. Ironically, our inability to replace human judgment is the most important limitation in the entire digital asset conversation—because while ownership can be digitized, governance, with its inherently human only elements, cannot be automated away. Decision making requires people. Risk management is a people business. Accountability is evergreen. There is no alternative.

Tokenization has indeed captured the imagination of markets, technologists, and investors alike. By converting real-world assets—such as gold, silver, and other metals—into digital tokens on a blockchain, proponents promise greater transparency, liquidity, and accessibility. It is a compelling vision–one that is also incomplete. Why is that? Because behind every tokenized asset lies something far more fundamental than code: a system of trust, accountability, and decision-making called governance!

What Tokenization Actually Does—and Does Not Do

At its core, tokenization is a method of representation. A token may represent:

- A bar of gold in a vault

- A share of a mining project

- A claim on future production

The blockchain on the other hand provides:

- A ledger

- Transparency of transactions

- Immutable record-keeping

These are important innovations. Nevertheless, neither answer critical questions:

- Who verifies that the gold actually exists?

- Who ensures it is properly stored and insured?

- Who decides how a mining project allocates capital?

- Who steps in when something goes wrong?

These are not technical questions. They are governance questions.

The Illusion of “Trustless” Systems

One of the most common narratives in tokenization is the idea of a “trustless” system—one in which technology replaces the need for trust. This is misleading and here’s why.

Tokenized metals still depend on:

- Custodians

- Auditors

- Operators

- Issuers

Each of these actors introduces:

- Judgment

- Incentives

- Potential conflicts

Blockchain may reduce certain forms of risk, but it does not eliminate the need to trust: it simply shifts where that trust is placed. What’s worse, without excellence in governance the trust becomes more fragile and opaque–not less.

Where Governance Enters the Equation

Governance is not a theoretical construct. It is a practical framework that answers fundamental questions:

- Who is responsible for what?

- How are decisions made?

- How are risks monitored and managed?

- How are stakeholders protected?

In the context of tokenized metals, governance must address several layers:

1. Asset-Level Governance. Is the Underlying Asset:

- Real

- Properly stored

- Independently verified

2. Operational Governance. Are the Entities Involved:

- Competent

- Accountable

- Subject to oversight

3. Financial Governance. How are:

- Revenues managed

- Costs controlled

- Capital allocated

4. Disclosure and Transparency. Are investors receiving:

- Accurate information

- Timely updates

- Balanced reporting

These are the same governance questions that exist in traditional finance. Tokenization does not remove them. It amplifies them.

The Mining Parallel

The tokenization of metals ultimately connects back to physical mining. Before a token can represent gold or copper, that metal must be:

- Discovered

- Developed

- Extracted

Mining is capital-intensive, high-risk, and operationally complex. To paraphrase legendary natural resources investor, Rick Rule, weak governance in mining leads to poor outcomes—regardless of asset quality.

Projects fail not only because of geology, but because of:

- Poor capital discipline

- Lack of oversight

- Conflicts of interest

- Weak boards

Tokenization does not fix these problems. If anything, it can obscure them—by placing a digital layer over an imperfect foundation.

Governance as a Value Multiplier

When governance is strong, it does more than reduce risk. It creates value. In tokenized metals, strong governance can:

- Increase investor confidence

- Improve capital access

- Enhance credibility with institutions

- Support long-term sustainability

Investors are not simply buying tokens. They are buying the integrity of the system behind those tokens and that integrity is built through governance.

The Role of Boards and Oversight

At the center of governance is oversight of management. Boards and governing bodies must ensure that:

- Systems are functioning as intended

- Risks are identified and addressed

- Decisions are aligned with long-term value

In many tokenization discussions, governance is treated as secondary—an afterthought once the technology is in place. What a mistake! To be most effective governance must be designed in from the beginning—not added later.

The Risk of Getting It Wrong

The risks of weak governance in tokenized metals are significant:

- Misrepresentation of assets

- Operational failures

- Loss of investor confidence

- Regulatory intervention

In a worst-case scenario, technology can accelerate the spread of problems rather than contain them. A flawed system, once tokenized, becomes:

- More scalable

- More visible

- More fragile

Regulation Is Not a Substitute

Commentators may argue that regulation will fill the governance gap. That is not the job of the government, nor should it be. As a former government regulator I understand regulation is important—but it is not sufficient. Regulators:

- Set minimum standards

- Enforce compliance

They do not:

- Run companies

- Make daily decisions

- Replace effective boards

Building Governance into Tokenization

For tokenized metals to reach their potential, governance must be integrated into the design of the system. This includes:

- Clear roles and responsibilities

- Independent oversight

- Robust audit processes

- Transparent reporting

- Alignment of incentives

It also requires a shift in mindset, from technology-first, to structure-first.

What This Really Means

Tokenization is a powerful tool. It has the potential to reshape how assets are owned, traded, and accessed. However, it is not even a poor substitute for governance. Rather, it is a layer built on top of governance.

Get the governance right, and tokenization can enhance value, transparency, and trust. Get it wrong, and no amount of technology will compensate. Because in the end investors do not rely on code alone.

They rely on the people, structures, and decisions behind it. And guess what? Those are governed–not programmed.

Until next time,

Yogi Nelson (Nelson Hernandez)