You can own gold tokens on the blockchain. Many people do. You can track every transaction. You can see your balance instantly. It feels precise. Modern. Reliable. But one question changes everything: Where is the metal?

And just as important: Who verifies that it’s actually there?

Tokenization does many things well. It improves efficiency, transparency, and access. But it does not eliminate the need for custody, verification, and governance.

Blockchain can record ownership.

It cannot inspect vaults. It cannot audit inventory. It cannot confirm whether assets are unencumbered.

That responsibility falls to custodians, auditors, and governance structures.

“Proof of reserves” helps—but it is not a complete solution. It can confirm consistency, not necessarily reality. At the end of the day, trust has not disappeared. It has simply moved. And that raises a critical point:

Investors are not just buying a token—they are buying a system of trust behind it.

That system must be examined carefully. Because in tokenization, as in investing generally: Precision is not the same as truth.

You can own gold tokens on the blockchain. Yes, many do. After purchase, the tokens are visible on their screens. Using blockchain, gold token holders can track every transaction ever made. Of course, that feels precise. You might say modern… and perhaps reliable. However, one small, pesky question can ruin the moment: Where is the metal? And just as important: Who says it’s there—and how do you know?

Let’s not be naive—a token representing gold is only as good as the system that ensures that gold actually exists. Is that system a blockchain? Yes, but there is more to it—a lot more. The keys are custody, verification, and proof.

The Chain Behind the Token

Much has been written about blockchain as a trust mechanism—and for good reason. For instance, it records transactions. Blockchain also prevents double-spending. Moreover, it creates a permanent ledger. Everyone who understands blockchain agrees. However, when you understand the tech, you know blockchain does not:

Store gold

Inspect vaults

Verify bar numbers

Audit inventory

Those responsibilities fall to a chain of real-world actors:

Custodians (vault operators)

Auditors (third-party verifiers)

Issuers (token creators)

Sometimes insurers

Each of these introduces:

Judgment

Process risk

And each becomes a point where trust must be earned. Governance teaches what questions to ask. Let’s walk through that exercise now.

Custody: The First Point of Failure

What is the foundation of tokenization? If you answered custody, move to the front of the class. The basic premise is simple: a physical asset is stored somewhere, and a digital token represents it. However, life is often not simple, because beware—simplicity is often deceptive. Therefore, you need to ask penetrating questions such as:

Is the metal allocated or unallocated?

Is it segregated or pooled?

Is it held in a recognized vault?

Who has legal claim in the event of insolvency?

These are not technical distinctions. They are legal and operational realities.

A token holder may believe they “own gold,” but what they actually own depends entirely on the custody structure. In some cases, they own a specific bar, but it could instead be a claim on a pool or, worse yet, a claim on a claim. That’s why we need to discuss verification.

The Problem of Verification

Let us assume, for the moment, that the gold is indeed stored in a reputable vault. Fine. The next question becomes: Who verifies that it is actually there? This is where the concept of “proof” enters the discussion. Tokenized systems often rely on:

Periodic audits

Attestations

Internal reporting

These vary significantly in quality. For example, an audit typically involves:

Independent verification

Physical inspection

Reconciliation of records

By contrast, an attestation may simply confirms that a statement provided by management appears reasonable Those are not the same thing. Yet in many tokenized systems, the distinction is not clearly communicated. As is said in India, “what to do”? The answer: proof of reserves.

Proof of Reserves: A Partial Solution

In response to growing skepticism, many token issuers now promote “proof of reserves.” Promoters may try to present proof of reserves as a technological breakthrough. It’s not. In reality, it is a hybrid concept. Proof of reserves may show:

The number of tokens issued

The assets claimed to back them

But it does not always prove:

That the assets are unencumbered

That they are not pledged elsewhere

That they are held in the stated form

In other words: proof of reserves can confirm consistency—but not necessarily reality. Is it a step forward? You bet. When it comes to governance, there is no substitute for precision, and even that has its challenges, as explained below.

The Illusion of Precision

One of the more subtle, but real, risks in tokenized systems is the illusion of precision. After all, it’s a system built on a foundation of math and cryptography. A blockchain ledger may show:

Precise quantities

Exact timestamps

Strict ownership

This creates a sense of certainty. But precision in the digital layer does not guarantee accuracy in the physical layer. You can have perfect records of imperfect information

This is not a flaw in the technology. It is a limitation of what the technology can verify.

Trust Has Not Disappeared—It Has Moved

The idea of “trustless” systems suggests that trust is no longer required. Wrong. In reality, trust has not disappeared—it has simply moved. For the better? Maybe. Instead of trusting banks, you are trusting:

Custodians

Auditors

Issuers

The question is not whether trust exists. That question is evergreen. The questions are: Where does trust reside—and whether it is justified. Align those questions, and trust increases. Hence, we next examine alignment and misalignment.

When Custody and Governance Align

Strong systems recognize these limitations and address them directly. They incorporate:

Reputable, third-party vaults

Clear legal ownership structures

Regular, independent audits

Transparent reporting

More importantly, they establish:

Oversight mechanisms

Accountability frameworks

In such systems, custody is not just a function—it is governed. And governance ensures that:

Processes are followed

Risks are identified

Discrepancies are addressed

Misalignment–When Governance Fails

Weak systems tend to rely on:

Brand perception

Marketing language

Selective disclosure

They may may also emphasize:

Technology

Innovation

Accessibility

While minimizing discussion of:

Custody arrangements

Audit rigor

Legal structure

These are the systems where problems emerge. Not immediately. Eventually. And always. As an investor, your duty is to ask 100+ probing questions.

The Role of the Investor

This raises an uncomfortable reality: The burden of understanding often falls on the investor. Investors must ask:

Where is the asset?

Who holds it?

How is it verified?

What happens if something goes wrong?

These are not easy questions—but necessary ones. Without clear answers, the token becomes an assumption—not an asset. You know what they say about assumptions!

What Does It All Mean

Tokenization promises efficiency, transparency, and access. Awesome benefits. However, it does not eliminate the need for:

Custody

Verification

Governance

Judgment

Tokenization makes those elements more important. Once an asset is tokenized, it becomes:

Easier to trade

Faster to distribute

Simple to scale

Which also means weaknesses become magnified.

In conclusion the buyer is purchasing more than a token. Investors are buying a system of trust—a system that must be scrutinized, not assumed.

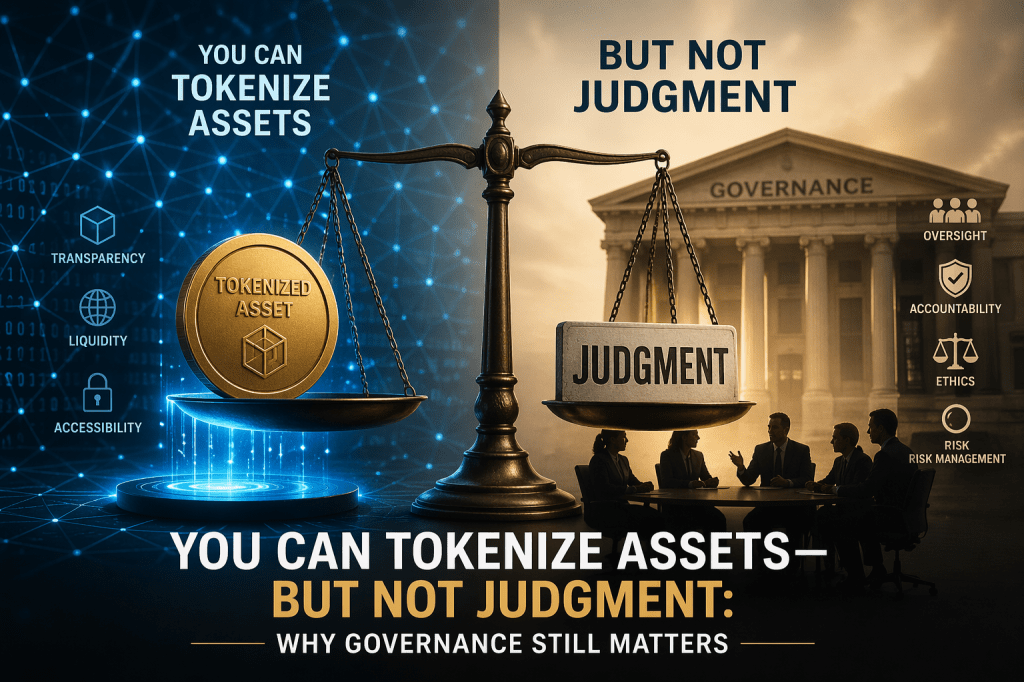

You can tokenize assets. You can tokenize gold, silver, and just about anything of value. But you cannot tokenize judgment. That may be the most important limitation in the entire digital asset conversation.

Tokenization promises transparency, liquidity, and accessibility. It’s a compelling vision—and one that is partially true. But behind every tokenized asset lies something far more fundamental than code: Governance.

Who verifies the asset exists? Who ensures it is properly stored? Who makes capital decisions? Who is accountable when things go wrong?

These are not technical questions. They are governance questions.

The idea of “trustless” systems is often misunderstood. Tokenization doesn’t eliminate trust—it simply shifts it. And without strong governance, that trust becomes more fragile, not less.

As tokenized metals evolve, the real challenge won’t be technological. It will be structural. Investors are not relying on code alone—they are relying on the people, systems, and decisions behind it. Those are governed—not programmed.

Can assets be tokenize? Absolutely yes. The more important question is, can judgement be tokenize? Absolutely not. Ironically, our inability to replace human judgment is the most important limitation in the entire digital asset conversation—because while ownership can be digitized, governance, with its inherently human only elements, cannot be automated away. Decision making requires people. Risk management is a people business. Accountability is evergreen. There is no alternative.

Tokenization has indeed captured the imagination of markets, technologists, and investors alike. By converting real-world assets—such as gold, silver, and other metals—into digital tokens on a blockchain, proponents promise greater transparency, liquidity, and accessibility. It is a compelling vision–one that is also incomplete. Why is that? Because behind every tokenized asset lies something far more fundamental than code: a system of trust, accountability, and decision-making called governance!

What Tokenization Actually Does—and Does Not Do

At its core, tokenization is a method of representation. A token may represent:

A bar of gold in a vault

A share of a mining project

A claim on future production

The blockchain on the other hand provides:

A ledger

Transparency of transactions

Immutable record-keeping

These are important innovations. Nevertheless, neither answer critical questions:

Who verifies that the gold actually exists?

Who ensures it is properly stored and insured?

Who decides how a mining project allocates capital?

Who steps in when something goes wrong?

These are not technical questions. They are governance questions.

The Illusion of “Trustless” Systems

One of the most common narratives in tokenization is the idea of a “trustless” system—one in which technology replaces the need for trust. This is misleading and here’s why.

Tokenized metals still depend on:

Custodians

Auditors

Operators

Issuers

Each of these actors introduces:

Judgment

Incentives

Potential conflicts

Blockchain may reduce certain forms of risk, but it does not eliminate the need to trust: it simply shifts where that trust is placed. What’s worse, without excellence in governance the trust becomes more fragile and opaque–not less.

Where Governance Enters the Equation

Governance is not a theoretical construct. It is a practical framework that answers fundamental questions:

Who is responsible for what?

How are decisions made?

How are risks monitored and managed?

How are stakeholders protected?

In the context of tokenized metals, governance must address several layers:

1. Asset-Level Governance. Is the Underlying Asset:

Real

Properly stored

Independently verified

2. Operational Governance. Are the Entities Involved:

Competent

Accountable

Subject to oversight

3. Financial Governance. How are:

Revenues managed

Costs controlled

Capital allocated

4. Disclosure and Transparency. Are investors receiving:

Accurate information

Timely updates

Balanced reporting

These are the same governance questions that exist in traditional finance. Tokenization does not remove them. It amplifies them.

The Mining Parallel

The tokenization of metals ultimately connects back to physical mining. Before a token can represent gold or copper, that metal must be:

Discovered

Developed

Extracted

Mining is capital-intensive, high-risk, and operationally complex. To paraphrase legendary natural resources investor, Rick Rule, weak governance in mining leads to poor outcomes—regardless of asset quality.

Projects fail not only because of geology, but because of:

Poor capital discipline

Lack of oversight

Conflicts of interest

Weak boards

Tokenization does not fix these problems. If anything, it can obscure them—by placing a digital layer over an imperfect foundation.

Governance as a Value Multiplier

When governance is strong, it does more than reduce risk. It creates value. In tokenized metals, strong governance can:

Increase investor confidence

Improve capital access

Enhance credibility with institutions

Support long-term sustainability

Investors are not simply buying tokens. They are buyingthe integrity of the system behind those tokens and that integrity is built through governance.

The Role of Boards and Oversight

At the center of governance is oversight of management. Boards and governing bodies must ensure that:

Systems are functioning as intended

Risks are identified and addressed

Decisions are aligned with long-term value

In many tokenization discussions, governance is treated as secondary—an afterthought once the technology is in place. What a mistake! To be most effective governance must bedesigned in from the beginning—not added later.

The Risk of Getting It Wrong

The risks of weak governance in tokenized metals are significant:

Misrepresentation of assets

Operational failures

Loss of investor confidence

Regulatory intervention

In a worst-case scenario, technology can accelerate the spread of problems rather than contain them. A flawed system, once tokenized, becomes:

More scalable

More visible

More fragile

Regulation Is Not a Substitute

Commentators may argue that regulation will fill the governance gap. That is not the job of the government, nor should it be. As a former government regulator I understand regulation is important—but it is not sufficient. Regulators:

Set minimum standards

Enforce compliance

They do not:

Run companies

Make daily decisions

Replace effective boards

Building Governance into Tokenization

For tokenized metals to reach their potential, governance must be integrated into the design of the system. This includes:

Clear roles and responsibilities

Independent oversight

Robust audit processes

Transparent reporting

Alignment of incentives

It also requires a shift in mindset, from technology-first, to structure-first.

What This Really Means

Tokenization is a powerful tool. It has the potential to reshape how assets are owned, traded, and accessed. However, it is not even a poor substitute for governance. Rather, it is a layer built on top of governance.

Get the governance right, and tokenization can enhance value, transparency, and trust. Get it wrong, and no amount of technology will compensate. Because in the end investors do not rely on code alone. They rely on the people, structures, and decisions behind it. And guess what? Those are governed–not programmed.

Why Junior Mining Boards Must Exercise Discipline When Raising Capital

Junior mining companies live on capital. No capital; no life. Unlike operating businesses that generate revenue from the sale of products, junior miners rely almost entirely on investor funding to advance their projects. Drilling programs, geological surveys, environmental studies, and technical reports all require capital long before a mine ever produces its first ounce of metal. The implication is clear: financing rounds are not simply financial events. They are governance events.

When a junior mining company raises capital—whether through private placements, strategic investments, or institutional participation—the board of directors must exercise disciplined oversight to ensure the financing process protects both the company and its shareholders.

Financing is the mother’s milk of exploration companies. Poor governance during financing rounds, however, can damage credibility in ways that are difficult, if not impossible, to repair.

In junior mining, financing is inevitable. Governance discipline determines whether it builds value—or erodes it.

Capital Formation in the Junior Mining Sector

Capital markets are the engine that powers the junior mining industry. Exploration companies raise funds repeatedly over the life cycle of a project. Early-stage drilling programs may require modest financing, while later phases, such as development, demand larger capital injections. Regardless of the phase, each financing round presents difficult questions for management and the board. Consider these examples:

How should the financing be structured?

What price should the shares be issued at?

Should insiders participate in the financing?

How much dilution is acceptable?

Which investors should be invited to participate?

These questions transcend financial decisions. They are governance decisions that affect fairness, transparency, shareholder trust, and thus long-term viability.

Pricing Discipline and Fairness

The price at which new shares are issued is a sensitive decision fraught with opportunities and pitfalls. In junior mining markets, financings are often priced at a discount to the prevailing market price. This practice can be necessary to attract investors, particularly in volatile commodity markets or during periods of weak market sentiment. However, the board must ensure that pricing decisions are reasonable and defensible.

Issuing shares at excessively discounted prices may dilute existing shareholders unnecessarily and raise questions about who benefits: new investors or the company? That is why directors should carefully evaluate:

Market conditions at the time of the financing

Comparable financings within the sector

The company’s capital requirements

The potential dilution impact on existing shareholders

Governance discipline requires that pricing decisions reflect the best interests of the company—not convenience.

Insider Participation

Financing rounds frequently include participation from insiders such as directors, officers, and major shareholders. And do not get me wrong—insider participation can be viewed positively. When insiders invest their own capital alongside other investors, it may signal confidence in the company’s prospects. Nevertheless, insider participation introduces governance considerations that must be handled carefully.

Boards must ensure that:

Insider participation is fully disclosed

Pricing and allocation decisions are fair

Conflicts of interest are properly managed

Independent directors review the transaction

Transparent governance processes help ensure that insider participation strengthens investor confidence rather than undermining it.

Allocation of Shares

Another governance challenge during financing rounds involves the allocation of shares among participating investors. This is a big deal and must be handled with care.

In highly oversubscribed financings, management may have significant discretion in deciding which investors receive allocations. Therefore, these decisions can have long-term implications for the company’s shareholder base. For example, the board may wish to encourage participation from:

Long-term institutional investors

Strategic partners

Industry specialists

Investors with expertise in the mining sector

Conversely, allocating significant shares to short-term speculators may create future volatility in the company’s shareholder base. Boards should therefore remain attentive to how capital is allocated and whether the resulting shareholder structure supports the company’s long-term objectives.

Disclosure and Transparency

Financing transactions must be accompanied by clear and accurate disclosure. Investors participating in a financing round expect transparency regarding the terms of the offering, the use of proceeds, and any participation by insiders. This is a non-negotiable standard. At a minimum, typical disclosure should include:

The price and size of the financing

The use of proceeds

Participation by directors or officers

Any special warrants or conversion features

Regulatory approvals required for the transaction

Transparent disclosure is not simply a regulatory obligation. It is a key element of market credibility. And never lose sight of why quality disclosures are essential: investors are far more likely to support companies that communicate financing decisions openly and clearly.

The Board’s Oversight Responsibility

Although management typically negotiates financing arrangements, the board of directors must exercise strict oversight over the process. Board oversight must include reviewing the structure of the financing, evaluating its fairness, and ensuring that conflicts of interest are properly managed.

In many cases, and to augment credibility with the market, independent directors may take the lead in reviewing the financing to ensure that the interests of existing shareholders are protected. Financing deals raise dozens of questions, but at a minimum the board should ask fundamental questions during financing discussions:

Does the financing structure serve the long-term interests of the company?

Are the terms fair to existing shareholders?

Have conflicts of interest been properly disclosed and addressed?

Is the company raising the appropriate amount of capital relative to its needs?

Avoiding Governance Pitfalls

Financing rounds can expose junior mining companies to several governance pitfalls if not managed carefully. The possible scenarios are almost endless. Nevertheless, the pitfalls generally fall into several categories. For example: Are existing shareholders being diluted excessively? Is there preferential treatment of insider investors? Are disclosure practices transparent or opaque? Is there proper alignment between financing size and project needs?

If those questions—or similar ones—cannot be answered in the affirmative, the company may be headed toward a governance pitfall. And remember: credibility is elusive once lost.

Governance and Market Reputation

Junior mining companies, in many respects, are no different from any other startup company—they depend heavily on investor confidence. Exploration companies may raise capital many times before a project reaches development or production. For this reason, reputation in capital markets is one of a company’s most valuable assets. Do not waste it.

Companies that demonstrate disciplined governance during financing rounds build credibility with investors, analysts, and industry participants. Conversely, companies that conduct poorly structured financings may find it increasingly difficult to attract capital in the future. In other words, governance during financing rounds influences not only the current financing—but also the company’s ability to raise capital in the years ahead.

Final Thoughts

Financing rounds are among the most consequential decisions that junior mining boards will oversee. Get it right and thrive; get it wrong and watch value slide. While management may lead the capital raising process, the board bears responsibility for ensuring that the financing is structured fairly, disclosed transparently, and aligned with the long-term interests of shareholders.

In the junior mining industry, capital is precious. So is credibility. Boards that exercise governance discipline during financing rounds protect both. In a sector where companies depend on investor trust long before revenue arrives, that discipline can make all the difference.