Tokenization promises a lot—speed, transparency, global access, and the ability to move physical assets at digital speed. But there’s one uncomfortable question the space doesn’t like to linger on:

Who’s on the other side of the trade?

Liquidity is not about technology. It’s about participation.

An asset can be perfectly tokenized and still be difficult to buy or sell in meaningful size without moving the price. When that happens, confidence erodes quickly—no matter how elegant the blockchain design may be.

This is especially true in tokenized metals.

Gold begins with a structural advantage: deep global markets, standardized bars, central bank participation, and centuries of trust. Silver follows, but with more volatility. Other metals—platinum, palladium, and especially rhodium—face much steeper liquidity challenges that tokenization alone cannot solve.

The hard truth is this: Tokenization digitizes access. Liquidity determines usability.

That’s where market makers, institutional participation, predictable redemption, and market structure come into play. Liquidity isn’t created by opening the doors—it’s earned through trust, depth, and consistent participation.

Technology helps. But economics still has the final say.

If you’re interested in where tokenized metals realistically stand today—and what would need to change for them to reach global volume—I explore the liquidity question in depth in my latest long-form piece. Yogi Nelson

Part of an ongoing, long-form series examining the tokenization of precious metals—one of the few sustained efforts to explore custody, liquidity, redemption, and market structure throughout 2026.

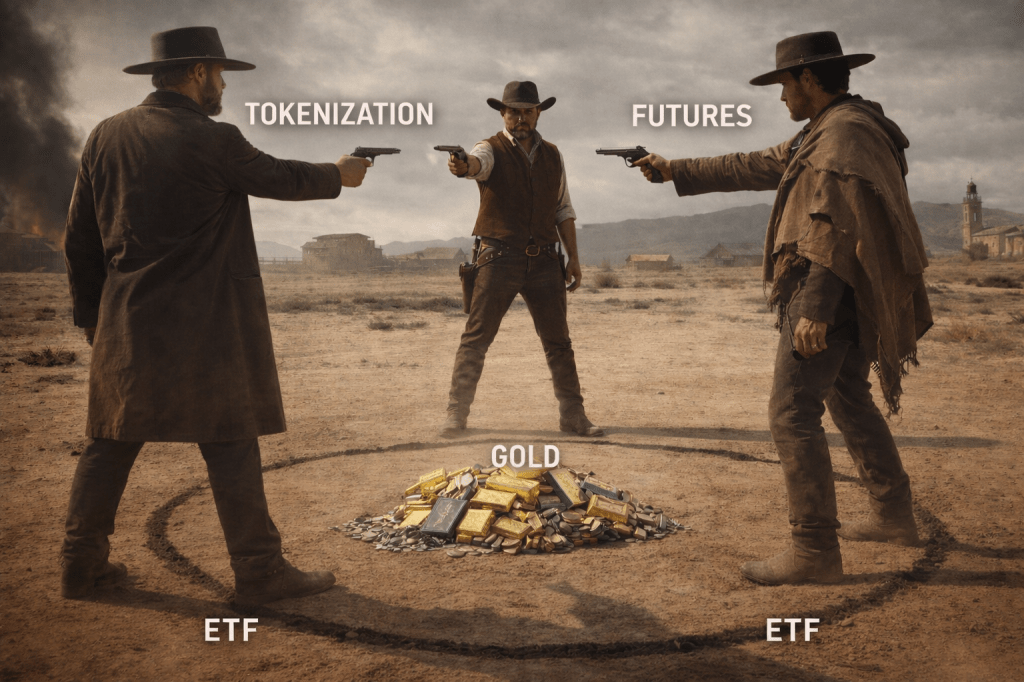

There are three primary ways investors gain exposure to gold today: physical ownership, ETFs, and futures. Each exists for a reason. Each solves a different problem. And each comes with its own tradeoffs.

Tokenized metals add a fourth dimension—not by replacing these structures, but by forcing a more precise question:

Are you buying ownership, or are you buying exposure?

ETFs deliver efficient price exposure, but usually through pooled structures with limited redemption rights. Futures provide price discovery and hedging power, but they are contracts—not assets. Physical gold offers direct ownership, but comes with real-world friction: storage, insurance, and logistics.

Tokenization sits between these models. When structured properly, it can combine digital transferability with claims on physically vaulted metal. When structured poorly, it becomes just another derivative with a new label.

That distinction matters—especially for institutions. What they care about is not speculation, but market plumbing: settlement, custody, collateral mobility, auditability, and counterparty risk. Tokenization becomes interesting only when it improves those foundations.

The future of metals is not a shootout between ETFs, futures, and tokenization. It is a question of which structures best serve ownership, transparency, and settlement in a digital economy.

— Yogi Nelson

This post is part of an ongoing weekly series on the tokenization of precious metals, published on BlockchainAIForum and LinkedIn, examining custody, regulation, issuer structure, and settlement infrastructure.

“A token isn’t gold; the structure behind it is—and that’s where the real competition in tokenized metals is happening.” Yogi Nelson

Tokenization is no longer theoretical. By 2026, it has become a defining theme across finance—from equities and bonds to commodities. When it comes to precious metals, however, how tokenization is implemented matters far more than the token itself.

A token is not gold. The structure behind the token is the asset.

That means custody, audits, redemption rights, regulatory posture, and market integration matter far more than marketing claims.

In reviewing the leading tokenized gold issuers operating today, one thing becomes clear: there is no single “winner.” Instead, each issuer is running a different race—toward a different vision of what tokenized metals should be.

Here’s how the field lines up:

CACHE Gold → transparency and auditability

Comtech Gold → trade and settlement infrastructure

Kinesis → re-monetizing gold and silver as money

Paxos (PAXG) → institutional compliance and regulatory clarity

T-Gold (SchiffGold) → sound-money preservation

Tether Gold (XAUT) → liquidity and global reach

Tokenization is not a template. It’s a toolkit.

Some issuers optimize for institutions. Others for velocity, trade finance, or individual ownership. The common thread is this: tokenization is shifting precious metals from static holdings toward programmable financial infrastructure.

That is the real story—and why issuer design now matters more than the token symbol itself.

“A token isn’t gold; the structure behind it is—and that’s where the real competition in tokenized metals is happening”. Yogi Nelson

Coinbase CEO, Brian Armstrong, and Larry Fink, Blackrock CEO, both agree–tokenization of assets is the theme for 2026. Both understand tokenization has moved from theory to practice. Tokenization of gold is at the forefront of this tsunami. Yet regulatory posture, and market integration matter far more than marketing claims.

This article provides a clear, structured comparison of the leading tokenized precious metal issuers operating in 2026. The goal is not to rank them by hype or price performance, but to evaluate them by structure, credibility, and long-term viability.

Why Issuer Structure Matters More Than the Token Itself

Tokenized precious metals are often discussed as if the token is the asset. It is not. The real asset is the legal and custodial framework behind the token. Please remember this!

Considering a tokenized purchase? Here are a few questions to ask when conducting your due diligence:

Who holds the metal, and where?

Is the metal fully allocated and segregated?

Who audits the reserves, and how often?

What legal rights does a token holder actually have?

Can the token be redeemed for physical metal?

Is the issuer regulated — and in which jurisdictions?

In 2026, the strongest issuers are those that treat tokenization as financial infrastructure, not merely as a crypto product. I can’t emphasize this point enough. With that as background, let’s examine the best-known gold token issuers. They are listed in alphabetical order, not from “best” to “worse”.

CACHE Gold approaches tokenization from a simple but demanding premise: trust must be visible. Rather than leading with liquidity or ideological framing, CACHE positions transparency and auditability as its core value proposition.

Each CGT token represents allocated physical gold stored in professional vaults across multiple jurisdictions. CACHE publishes detailed bar lists and emphasizes independent third-party audits, reinforcing the principle that token holders should be able to verify backing without relying on institutional reputation alone. Trust but verify!

Tokenization here functions as a disclosure mechanism. The blockchain is not used to create financial complexity, but to make existing bullion practices more observable and accountable. This appeals to users who are less interested in DeFi composability and more concerned with proof-of-reserves discipline. Smart idea.

The tradeoff is scale. CACHE operates within a smaller ecosystem, with lower secondary-market liquidity and fewer exchange integrations than the largest issuers. Its design prioritizes clarity over velocity.

Best suited for: investors who value strong transparency, auditability, and vault diversification over liquidity or speculative activity.

Comtech Gold (CGO): Tokenization Built for Trade and Settlement

Comtech Gold represents a distinctly utilitarian vision of tokenized metals. Rather than framing gold as an investment product, Comtech positions tokenized gold as commercial infrastructure—designed to support commodity trade, collateralization, and settlement in regulated environments. They found a nice niche.

CGO tokens are issued within commodity-exchange and trade-finance frameworks, particularly in emerging and trade-focused jurisdictions. Gold is held with approved custodians, and token issuance aligns closely with existing regulatory regimes governing physical commodities.

Tokenization here improves settlement efficiency, traceability, and operational speed without attempting to disrupt the logic of trade markets. Comtech does not pursue broad retail adoption or DeFi composability; its focus is narrow by design.

This specialization limits visibility among Western retail investors and reduces global liquidity. But within its intended domain, Comtech’s approach is structurally coherent.

Best suited for: trade finance, commodity settlement, and emerging-market use cases where regulatory alignment and real-economy integration matter most.

Kinesis (KAU, KAG): Tokenized Metals as a Monetary System

Kinesis treats tokenization not as a feature, but as monetary architecture. Its gold (KAU) and silver (KAG) tokens are designed to circulate, settle, and function as money rather than static investment instruments.

Each token is backed by allocated physical metal stored in professional vaults across multiple jurisdictions. What distinguishes Kinesis is its yield-sharing model, which redistributes transaction fees to users who hold and actively use the metals. This design emphasizes velocity—a deliberate attempt to restore monetary function to precious metals. Back to the future?

Tokenization in Kinesis is therefore systemic. The blockchain coordinates ownership, settlement, and incentive distribution, creating an ecosystem where metals are meant to move.

This ambition introduces complexity. Users must understand system mechanics, fee flows, and governance. Institutional adoption has been slower than for simpler, custody-centric issuers.

Best suited for: users who believe precious metals should function as money, not merely as stores of value–an uphill climb.

Paxos remains one of the most institutionally credible issuers in the tokenized metals space, largely because it separates bullion standards from financial regulation with precision.

Each PAXG token represents ownership of one fine troy ounce of allocated physical gold. The gold conforms to London Bullion Market Association (LBMA) Good Delivery standards, ensuring bullion quality and refinery credibility. Importantly, LBMA sets market standards; it does not regulate issuers.

Regulatory oversight applies instead to Paxos itself, which operates under supervision by the New York Department of Financial Services (NYDFS). This dual structure—LBMA-standard bullion combined with NYDFS-regulated issuance—has made PAXG particularly attractive to institutions requiring legal clarity and compliance discipline.

PAXG emphasizes traceability, auditability, and redemption integrity. Each token can be linked to a specific gold bar, and attestations confirm full backing.

The tradeoff is flexibility. PAXG is gold-only, closely tied to U.S. regulatory jurisdiction, and less optimized for crypto-native experimentation.

Best suited for: institutions and regulated investors prioritizing legal certainty and bullion-market credibility.

T-Gold (SchiffGold): Sound-Money Tokenization with a Preservation Bias

Schiff Gold’s T-Gold reflects a philosophy-driven approach to tokenization. Rather than treating gold as a financial primitive to be re-engineered, T-Gold positions tokenization as a modern wrapper around traditional bullion ownership.

T-Gold represents allocated physical gold held with professional custodians, integrated into SchiffGold’s broader bullion ecosystem. The emphasis is preservation, ownership, and monetary discipline rather than yield or liquidity engineering.

Tokenization here improves portability and auditability without altering gold’s role as sound money. This clarity appeals strongly to investors already aligned with macro-oriented or anti-debasement narrative–a growing segment of the market.

Liquidity and secondary-market integration remain more limited than with larger issuers, and institutional settlement use cases are not the primary focus.

Best suited for: investors who prioritize sound-money principles and long-term wealth preservation.

Tether Gold (XAUT): Liquidity-First Tokenization at Global Scale

Tether’s XAUT represents a liquidity-first approach to tokenized gold. Each token corresponds to one fine troy ounce of allocated gold held in Swiss vaults, with redemption mechanisms available for larger holders.

What distinguishes XAUT is distribution and market depth. It is widely integrated across exchanges, wallets, and crypto-native platforms, often exhibiting greater secondary-market liquidity than competing gold tokens.

XAUT operates largely outside U.S. regulatory frameworks, offering flexibility and global reach but less formal oversight. Tokenization here is pragmatic: gold is treated as a stable, functional asset that can move at internet speed.

Best suited for: globally distributed, crypto-native users who value liquidity and accessibility over regulatory conservatism.

Key Comparison Themes

Across issuers, several patterns emerge:

Custody quality is table stakes; allocation and segregation are non-negotiable.

Redemption rights distinguish true tokenization from synthetic exposure.

Regulatory posture shapes who can use a token—and how.

Narrative coherence matters; the strongest issuers know why they tokenize.

Conclusion: Tokenization Is a Toolkit, not a Template

There is no single “best” tokenized precious metal issuer in 2026. Instead, there are clear leaders within distinct philosophies:

CACHE → transparency and auditability

Comtech Gold → trade and settlement

Kinesis → monetary re-engineering

Paxos → institutional compliance

T-Gold → sound-money preservation

Tether Gold → liquidity and reach

Tokenization is no longer about digitizing metal for novelty. It is about how metal-backed trust is structured, verified, and deployed in a programmable financial world.

That is the real story—and why issuer design now matters more than the token itself.

Gold tells the story of money. Silver tells the story of versatility. Palladium tells the story of technology, regulation, and fragility.

Long before catalytic converters made palladium famous, it was already a high-tech metal—used in electronics, chemical catalysis, and dentistry. What changed everything was environmental regulation. As emissions standards tightened, palladium became indispensable to gasoline-powered vehicles, eventually accounting for roughly 80% of global demand.

At the same time, supply remained extremely constrained. Palladium is mined primarily as a byproduct, with production concentrated in just two nations. That combination—industrial necessity and limited supply—has made palladium one of the most volatile precious metals of the past two decades.

This is precisely why palladium is a compelling candidate for tokenization.

Tokenized palladium can provide: • Transparent, on-chain ownership • Faster settlement in volatile markets • Fractional access to a scarce industrial asset • Improved supply-chain visibility

Unlike traditional futures or ETFs, tokenization is not synthetic exposure layered on top of complexity. It is direct, verifiable access to a real-world metal that modern technology depends on.

Palladium is not a monetary metal. It does not rely on mythology or tradition. Its value comes from physics, chemistry, and regulation—and in a high-tech age, that makes it a natural fit for blockchain-based infrastructure.

Tokenized palladium is not about hype. It is about alignment—between physical reality and digital systems.