Exploring the intersection of metals, tokenization and governance with Yogi Nelson

Author: Yogi Nelson

Hello, I'm Yogi Nelson. Reading, writing, and learning have always been my passions. For 33 years I worked in the public sector in the fields of city planning, housing, real estate, and finance. I retired in 2017 and travel extensively through Asia while dedicating myself to yoga. In 2020, I decided to dive into blockchain and crypto and now artificial intelligence. Join me as I answer your questions on these topics. As a bonus, I include proverbs from my upcoming book, "Global Wisdom: Proverbs from Every Nation", nano size comments related to one of my travel adventures and fun facts from different countries.

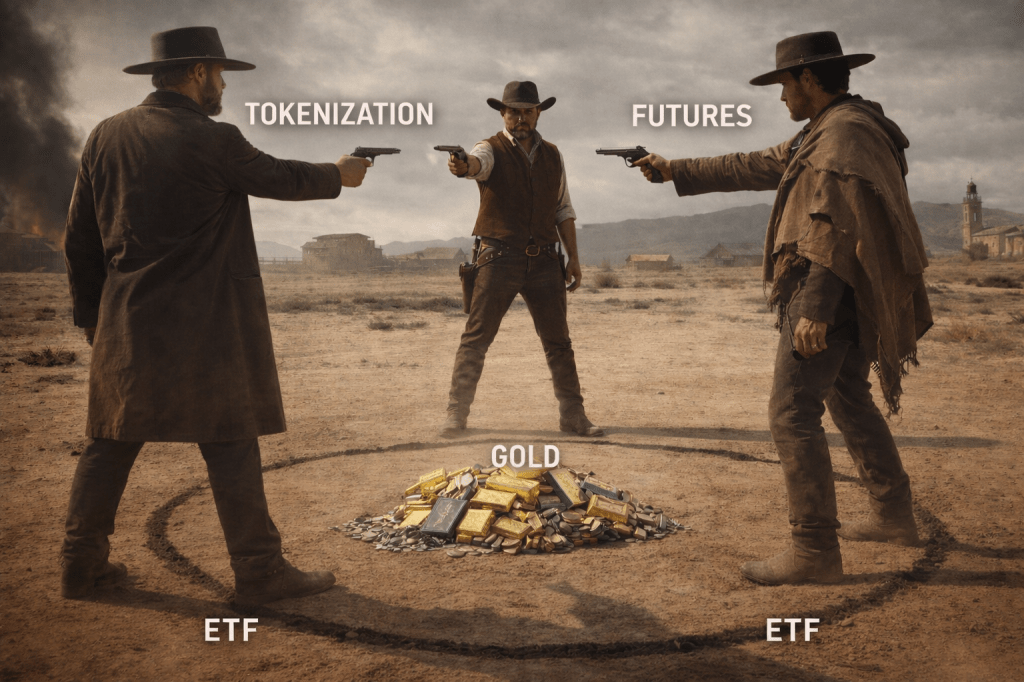

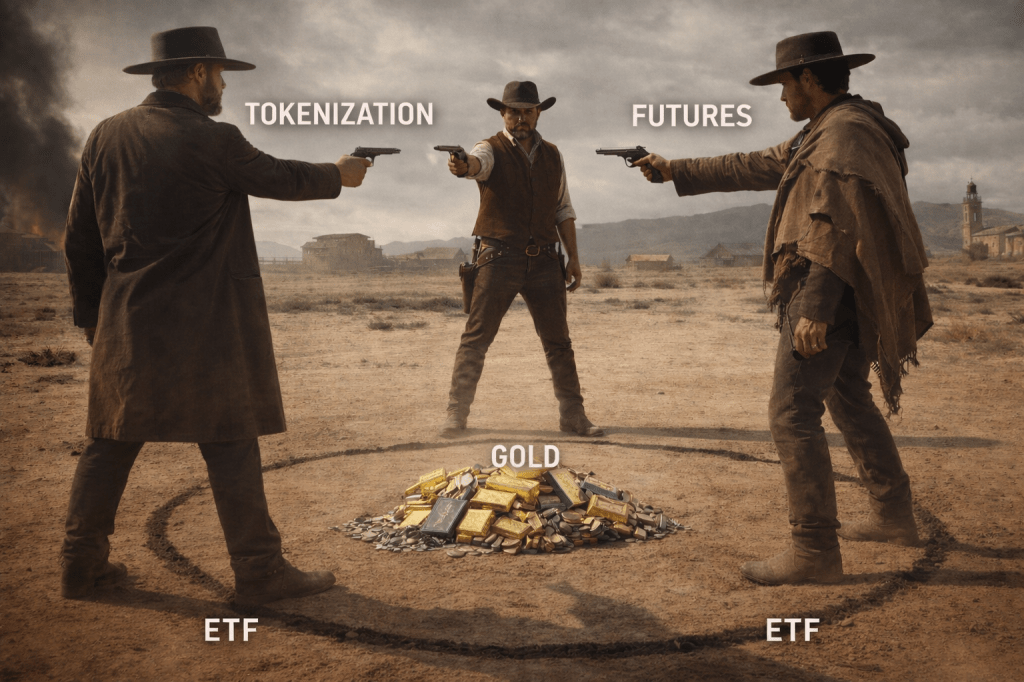

There are three primary ways investors gain exposure to gold today: physical ownership, ETFs, and futures. Each exists for a reason. Each solves a different problem. And each comes with its own tradeoffs.

Tokenized metals add a fourth dimension—not by replacing these structures, but by forcing a more precise question:

Are you buying ownership, or are you buying exposure?

ETFs deliver efficient price exposure, but usually through pooled structures with limited redemption rights. Futures provide price discovery and hedging power, but they are contracts—not assets. Physical gold offers direct ownership, but comes with real-world friction: storage, insurance, and logistics.

Tokenization sits between these models. When structured properly, it can combine digital transferability with claims on physically vaulted metal. When structured poorly, it becomes just another derivative with a new label.

That distinction matters—especially for institutions. What they care about is not speculation, but market plumbing: settlement, custody, collateral mobility, auditability, and counterparty risk. Tokenization becomes interesting only when it improves those foundations.

The future of metals is not a shootout between ETFs, futures, and tokenization. It is a question of which structures best serve ownership, transparency, and settlement in a digital economy.

— Yogi Nelson

This post is part of an ongoing weekly series on the tokenization of precious metals, published on BlockchainAIForum and LinkedIn, examining custody, regulation, issuer structure, and settlement infrastructure.

In the early stages of a junior mining company, the focus is understandably technical. Geological potential, drill programs, resource estimates, and exploration targets dominate discussions among management teams and investors alike. Discovery is the catalyst that creates excitement and attracts initial capital. Obvious. Yet as companies evolve, another factor increasingly determines whether they can continue to raise capital and attract serious institutional investors. What is that factor? Governance, with a capital “G”!

In many junior mining companies, governance is viewed primarily as a regulatory requirement — a series of policies and disclosures necessary to satisfy stock exchanges, securities regulators, and auditors. It is sometimes treated as administrative overhead rather than strategic infrastructure. That’s unfortunate. This perspective overlooks an important reality of capital markets: investors price risk. Governance, when implemented thoughtfully and proportionately, reduces perceived risk. And when perceived risk declines, access to capital improves.

In this sense, governance functions as a value multiplier.

Investors increasingly view governance quality as a key factor in valuing junior mining companies

Credibility as Currency

Unlike producing mining companies, junior miners often operate for years without generating revenue. Exploration companies rely almost entirely on investor capital to finance drilling programs, geological analysis, permitting work, and feasibility studies.

Because revenue is absent, investors rely heavily on documentation, trust, and credibility when allocating capital. They must believe that management is deploying funds responsibly, that financial reporting is reliable, and that internal oversight mechanisms exist to prevent costly mistakes or conflicts of interest. Investors believe in management when and if governance structures signal that credibility.

A well-constructed board, functioning audit committee, clear internal controls, and transparent reporting practices reassure investors that capital will be managed with discipline. These signals may not appear on a geological map, but they influence financing decisions in very real ways.

The Cost of Capital Connection

For junior mining companies, capital is the lifeblood of operations. Exploration programs, environmental studies, engineering work, and permitting processes require substantial funding long before any production revenue is possible. Companies that demonstrate governance maturity often benefit from improved financing conditions. Investors are more comfortable participating in private placements, strategic partnerships, and project financing when governance frameworks are visible and credible.

This can translate into:

More consistent access to financing

Broader investor participation

Improved valuation stability

Stronger relationships with institutional investors

In practical terms, governance can influence the price at which companies raise capital and the reliability of their funding sources. When investors perceive governance weakness, the opposite occurs. Capital becomes more expensive, investor participation narrows, and financing windows become more difficult to access.

Governance and Strategic Optionality

Governance also affects a company’s long-term strategic flexibility. Let me explain.

Junior mining companies often aim to progress through several stages: exploration, resource definition, feasibility analysis, development partnerships, and ultimately production or acquisition by a larger mining company. At each stage, the company interacts with increasingly sophisticated stakeholders.

Strategic partners, institutional investors, and major mining companies evaluate more than geological potential. They examine board composition, financial controls, disclosure practices, and risk management frameworks. Companies that have already developed disciplined governance structures are easier to evaluate, easier to partner with, and easier to finance.

In contrast, companies that postpone governance development may find themselves scrambling to retrofit policies and oversight structures precisely when potential partners are conducting due diligence.

Strong governance, implemented early, expands strategic options later. Keep that in mind.

Proportionate Governance for Small Companies

It is important to emphasize that governance does not mean bureaucracy.

Junior mining companies typically operate with lean teams and limited administrative capacity. Governance systems designed for multinational producers would be unnecessarily burdensome for early-stage explorers. What is needed is effective governance that is proportionate. Effective governance focuses on a small number of essential elements:

Independent board oversight

Clear financial reporting discipline

Basic internal controls over cash and expenditures

Transparent handling of related-party transactions

Thoughtful risk management and disclosure

These elements do not require large teams or expensive infrastructure. They require clarity, consistency, and leadership commitment.

Governance as Leadership Signal

Perhaps the most important function of governance in junior mining is the signal it sends about leadership culture. Companies that embrace governance early demonstrate that management and the board take stewardship responsibilities seriously. That message flows throughout the organization. They communicate that shareholder capital will be treated with care and that transparency is valued even during challenging periods.

This leadership signal becomes particularly important during moments of stress — when exploration results disappoint, commodity markets weaken, or financing conditions tighten. During such periods, investors gravitate toward companies that demonstrate discipline, accountability, and openness. Governance, in other words, reinforces confidence when it is most needed.

Building Governance Early

The most effective junior mining companies do not wait until they approach production or institutional financing to develop governance frameworks. That can often be too late. Smart miners incorporate governance as they evolve while their organizations are expanding.

Early governance adoption provides several advantages:

It builds credibility with investors from the outset

It prevents governance gaps from emerging as companies grow

It prepares companies for future partnerships and financing

It establishes internal discipline that supports operational efficiency

A Strategic Perspective

Ultimately, governance should not be viewed as an administrative requirement imposed from outside the organization. It is a strategic tool that strengthens the company’s ability to attract capital, manage risk, and pursue long-term opportunities. For junior mining companies operating in uncertain markets and capital-intensive environments, those advantages are significant.

Good geology creates potential. Good governance helps convert that potential into sustained investor confidence. And in the junior mining sector, investor confidence is often the decisive factor that allows companies to move from promising exploration stories to institutionally credible enterprises.

For decades, investors have gained exposure to precious metals and other hard assets through financial instruments designed for liquidity and scale rather than direct ownership. Exchange-traded funds and futures contracts made metals easier to trade, hedge, and price—but they also introduced layers of abstraction that separate investors from the underlying asset.

Tokenized metals reintroduce the question that those instruments largely set aside: what does it actually mean to own a hard asset?

Physical ownership implies custody, storage, insurance, and legal title. ETFs typically offer price exposure through pooled structures, with limited or no direct redemption for most investors. Futures markets facilitate price discovery and risk management, but they are contracts, not ownership vehicles. Tokenization, when structured properly, attempts to bridge these models—combining digital transferability with claims on physically vaulted metal.

This article compares tokenized metals directly with ETFs and futures by focusing on ownership rather than performance. The goal is not to argue that one model replaces the others, but to clarify how each structure works, what rights it confers, and what risks it introduces. Only by understanding these distinctions can investors and institutions evaluate where tokenization meaningfully changes market structure—and where it does not. Let’s now talk hard assets!

Hard Assets: Direct Ownership, Direct Responsibility

Hard assets are tangible, physical assets with intrinsic value. In the metals context, this means gold, silver, platinum, palladium, and other mined materials that must be refined, transported, stored, insured, and legally owned. Land ownership is a hard asset, but outside the scope of this series.

Traditional hard-asset ownership is conceptually simple: you own the metal. That ownership may be expressed through physical possession or through a custodial relationship with a vaulting provider, but the legal title is clear. The asset exists independently of any financial system.

The tradeoff is friction. Friction refers to the operational, financial, and logistical burdens associated with physical ownership—storage fees, insurance costs, transport limitations, slower settlement, and reduced liquidity. These frictions do not negate ownership, but they make hard assets less convenient to use within modern, fast-moving financial markets.

Hard assets provide certainty of ownership, but they do not scale easily in a global, digital system. That limitation is precisely what led to financial intermediaries.

ETFs: Exposure Without Possession

Exchange-traded funds revolutionized access to precious metals. Gold ETFs, in particular, allowed investors to gain exposure to gold prices using familiar brokerage accounts, with tight spreads and deep liquidity. ETFs excel at what they are designed to do:

Provide efficient price exposure

Integrate into regulated financial markets

Support institutional-scale liquidity

However, ETFs fundamentally change the ownership relationship. Most ETF holders do not own specific metal bars. They own shares in a trust or fund that holds metal through custodians and sub-custodians. Physical redemption is usually limited to authorized participants, not retail investors.

In practical terms, ETFs are financial exposure instruments, not ownership instruments. They track price movements effectively, but they intentionally abstract away custody, title, and delivery.

Futures Markets: Contracts, Not Assets

Futures markets serve a different purpose altogether. They are designed for:

Price discovery

Hedging

Risk transfer

Leverage

Futures contracts are agreements to buy or sell an asset at a future date, typically cash-settled or rolled forward. While physical delivery mechanisms exist, the vast majority of futures contracts never result in delivery.

Ownership is not the goal of futures markets. Exposure and risk management are. This makes futures indispensable to global markets, but unsuitable as ownership vehicles.

Global Markets: Scale at the Cost of Transparency

At the highest level, metals trade through global market infrastructure designed to support enormous volume and systemic stability. This infrastructure includes clearinghouses, central counterparties, and settlement networks such as the CME Clearing House, LCH, and international central securities depositories.

These entities perform critical functions: netting trades, managing counterparty risk, enforcing margin requirements, and ensuring settlement finality. Without them, global markets would not function.

However, this scale introduces distance. Ownership chains can involve multiple intermediaries—brokers, custodians, clearing members, and settlement agents—each adding legal and operational layers. End investors often rely on contractual assurances rather than direct visibility into custody or underlying assets.

This architecture prioritizes efficiency and stability, but it does so by design at the expense of transparency and direct ownership clarity.

Where Tokenized Metals Enter the Picture

Tokenization is often misunderstood as simply “putting gold on a blockchain.” In reality, tokenization is about restructuring ownership and settlement, not eliminating markets.

Tokenized metals attempt to:

Represent allocated physical metal digitally

Preserve custody and redemption rights

Enable peer-to-peer transfer

Reduce unnecessary intermediaries

Improve transparency

When designed properly, tokenization does not add another abstraction. It compresses existing layers by creating a single coordinated system that links physical custody, legal ownership, and transferability.

That coordinated system is tokenization implemented via a blockchain. The blockchain serves as the shared ledger that synchronizes ownership records, issuance, transfers, and redemptions, while the physical metal remains securely vaulted off-chain.

Whether tokenization succeeds depends entirely on how well this coordination is executed.

Tokenized Metals vs ETFs and Futures

The comparison becomes clearer when framed through ownership.

Ownership

Hard assets: Direct legal ownership

ETFs: Indirect exposure via fund shares

Futures: Contractual exposure

Tokenized metals: Potential direct ownership via digital representation

Liquidity

Hard assets: Low

ETFs: High

Futures: Very high

Tokenized metals: Variable, developing

Transparency

Hard assets: High at custody level

ETFs: Limited for end holders

Futures: Market-level transparency, not asset-level

Tokenized metals: High if properly designed

Redemption

Hard assets: Immediate

ETFs: Restricted

Futures: Rare

Tokenized metals: Platform-dependent

Taken together, tokenization does not automatically outperform ETFs or futures. Instead, it offers a different balance—trading some of the convenience of ETFs and the leverage of futures for improved ownership clarity, transparency, and settlement flexibility. This is why tokenized metals should not be viewed as replacements, but as alternatives optimized for different priorities.

Is Tokenization Just Another Derivative?

This is the central question—and the answer depends entirely on structure.

If a token:

Is not redeemable

Is backed by unallocated metal

Has opaque custody

Functions purely as price exposure

Then it is simply another derivative, regardless of blockchain branding.

However, tokenization can represent something fundamentally different. Consider the tokenization of land or real estate. When property is tokenized properly, the token does not represent price exposure—it represents legal title or enforceable claims on ownership, recorded digitally.

The same principle applies to metals. When a token represents allocated, uniquely identified metal with enforceable redemption rights, it functions as a digital ownership wrapper, not a derivative.

The distinction is not academic. It determines whether tokenization is merely financial engineering—or a genuine evolution in how ownership is recorded and transferred.

Why Institutions Care About Ownership Structure

Institutions already have access to ETFs and futures. They do not need tokenization for exposure. What they care about instead is market plumbing. And what is market plumbing? Market plumbing refers to the foundational systems that make markets function reliably:

Clearing and settlement

Custody and safekeeping

Collateral mobility

Reconciliation and auditability

Counterparty risk management

Cross-border interoperability

Tokenized metals become interesting to institutions when they improve this plumbing—by reducing settlement times, enhancing transparency, enabling programmable collateral, and simplifying reconciliation. In this sense, tokenization competes not on price or speculation, but on infrastructure efficiency.

Blockchain as Infrastructure, Not Ideology

The most credible tokenized metal platforms treat blockchain as infrastructure, not marketing. Public blockchains provide:

Immutable ownership records

Transparent issuance and supply tracking

Programmable transfer and settlement

Reduced reconciliation complexity

They do not replace vaults, insurers, or auditors. They coordinate them. This is what differentiates tokenization from earlier financial abstractions. ETFs and futures abstract ownership. Tokenization, at its best, re-architects it.

Global Markets Are Not Being Replaced

Tokenization will not replace ETFs, futures, or global commodity markets. Those systems exist because they solve real problems at scale. What tokenization can do is:

Offer alternatives for ownership-centric use cases

Complement existing markets

Improve settlement and transparency at the margins

Over time, those margins matter.

Conclusion: Understanding How Ownership Really Works

Hard assets, ETFs, futures, and tokenized metals are not competitors in a zero-sum sense. They are different tools, optimized for different purposes.

Tokenization does not eliminate abstraction. It challenges unnecessary abstraction. Its success will depend not on blockchain enthusiasm, but on custody, redemption, audits, and legal clarity. In that sense, tokenized metals are not a rebellion against markets—they are an evolution within them.

Understanding how ownership really works is the first step toward deciding where tokenization truly belongs.

Until next time,

Yogi Nelson

This article is part of an ongoing weekly series on the tokenization of precious metals, published on BlockchainAIForum and LinkedIn, examining custody, regulation, issuer structure, and settlement infrastructure.

Junior mining companies operate in one of the most, perhaps these most, capital-intensive, risk-exposed, and credibility-sensitive sectors in the global economy. They raise money before revenue. Moreover, they make technical promises before production. If that were enough, miners operate in jurisdictions where regulatory, environmental, and political variables can change quickly. And they do all of this, out of necessity, with lean teams and limited administrative and management infrastructure.

In that environment, governance is often viewed as an obligation — a regulatory requirement to satisfy exchanges, securities commissions, or auditors. Too frequently it becomes a checklist exercise. That perspective is shortsighted. In mining governance is not overhead. It is a strategic asset.

Strong governance frameworks help junior mining companies navigate risk, attract investment, and build enduring companies.

Over the next ten weeks, this series will explore how thoughtful governance and disciplined compliance frameworks can materially improve resilience, investor confidence, and long-term value creation in junior mining companies. The objective is not to advocate bureaucracy. To the contrary. It’s to demonstrate how structured oversight strengthens execution, reduces preventable risk, and positions companies for institutional capital.

This series is designed for directors, CEOs, CFOs, compliance officers, and serious investors who understand that governance is inseparable from capital formation. Below is an overview of what readers can expect.

1. Governance as a Value Multiplier in Junior Mining

We begin by reframing governance from a cost center to a value multiplier. Markets reward credibility. Institutions allocate capital where risk is understood and managed. Junior mining companies that articulate clear oversight structures, internal controls, and transparent reporting reduce perceived risk — and perceived risk directly affects valuation. In a business where risks are ubiquitous, strong governance enhances shareholder value.

This article will examine how governance maturity influences financing terms, investor retention, and strategic optionality.

2. Board Composition: Independence Versus Operational Expertise

Junior mining boards are often composed of geologists, founders, or major shareholders. Technical depth is essential — but independence and financial oversight are equally critical.

What true board independence means in a small company

How to balance technical knowledge with governance competence

When adding an independent director materially changes investor perception

The goal is not to replace industry expertise, but to complement it with structured oversight.

3. Audit Committees in Pre-Production Companies

Many early-stage companies view audit committees as formalities. Yet the absence of revenue does not eliminate financial risk–it often increases it!

The minimum functional standards for an effective audit committee

Oversight of cash management and exploration expenditures

Financial disclosure discipline in volatile commodity environments

A disciplined audit function signals seriousness to markets.

4. Internal Controls in Lean Organizations

Junior mining companies may operate with fewer than 25 employees. Segregation of duties can be challenging. Informal processes can emerge. We will explore how to implement practical internal controls without creating administrative burden, including:

Cash disbursement controls

Contract approval frameworks

Documentation protocols

Basic fraud prevention mechanisms

Strong controls do not require large teams. They require clarity.

5. Managing Related-Party Transactions in Small Teams

In closely held companies, related-party transactions are common. They are not inherently problematic — but they require transparency and structured oversight.

Disclosure best practices

Conflict-of-interest policies

Board review procedures

Protecting both insiders and minority shareholders

Proper handling of related-party matters strengthens trust.

6. CEO Oversight Without Micromanagement

Junior mining CEOs are often founders or highly technical leaders. Boards must support management while maintaining independent oversight.

Performance evaluation frameworks

Information rights and reporting cadence

Constructive challenge versus operational interference

Succession planning in early-stage companies

Healthy governance enhances leadership rather than constraining it.

7. ESG Reporting: Substance Versus Marketing

Environmental, social, and governance reporting has become unavoidable. Yet in junior mining, ESG narratives can outpace operational capacity.

8. Crisis Governance: When Exploration Results Disappoint

Commodity cycles fluctuate. Drill programs sometimes fail. Financing windows close unexpectedly.

Board protocols during operational setbacks

Disclosure discipline in adverse conditions

Liquidity oversight during market stress

Maintaining investor credibility during downturns

Crisis does not create governance weakness — it reveals it.

9. Jurisdictional Risk and Cross-Border Oversight

Many junior mining companies operate in Latin America, Africa, or other emerging markets. Cross-border operations introduce legal, political, and compliance complexity.

Anti-corruption controls

Local partner due diligence

Regulatory monitoring frameworks

Board-level oversight of geopolitical exposure

Risk awareness must extend beyond geology.

10. Governance Readiness for Institutional Capital

The final article in this series will synthesize the prior themes into a practical readiness framework.

Institutional investors assess:

Board independence

Financial reporting discipline

Risk management structures

ESG credibility

Executive compensation alignment

We will provide a structured checklist that junior mining boards can use to evaluate their governance posture before pursuing larger capital raises.

Why This Series Matters Now

Commodities are in a long-tend bull market. Miners that demonstrate strong governance attract higher quality investors. Investors increasingly differentiate between companies that treat governance as a formality and those that treat it as infrastructure. Junior mining companies do not need bureaucratic systems designed for multinational producers. They do need disciplined oversight tailored to their scale and stage of development.

The purpose of this series is practical: to offer clear frameworks, actionable insights, and governance standards that are achievable — even in lean organizations. Governance does not eliminate geological risk. It does not control commodity prices. But it reduces preventable errors, clarifies accountability, and strengthens credibility. And in capital markets, credibility compounds.

Over the next ten weeks, we will examine how junior mining companies can build governance systems that are proportionate, strategic, and aligned with long-term shareholder value.

The objective is not perfection.It is preparedness.

And in junior mining, preparedness often makes the difference between survival and sustainable growth.

That tension is where trust either holds—or breaks.

In tokenized metals, the blockchain is not the source of trust. The foundation remains physical and legal: professional vaulting, insurance, and proof-of-reserves. Tokenization does not replace these pillars; it exposes them.

Credible platforms answer hard questions:

Where is the metal actually stored?

Is it allocated and uniquely identified?

Who insures it—and for what risks?

How often are reserves audited?

Can tokens be redeemed for physical metal?

Building Trust with Blockchains

Blockchain adds transparency and coordination, but it cannot confirm physical reality on its own. That requires vault operators, insurers, auditors, and clear legal structures working together.

For institutions, this is not optional. Custody standards, audit discipline, redemption mechanics, and jurisdictional clarity are prerequisites—not features.

Tokenization does not create trust. It reveals whether trust already exists.

This is why the future of tokenized metals belongs not to the fastest platforms, but to those that treat trust as infrastructure—and build accordingly.

— Yogi Nelson

This post is part of an ongoing weekly series on the tokenization of precious metals, published on BlockchainAIForum and LinkedIn, examining custody, regulation, issuer structure, and settlement infrastructure.