by Yogi Nelson

Welcome to the BlockchainAIForum

In the world of cryptocurrencies and blockchain technology, many of the most successful projects are not run entirely by corporations in the traditional sense. Instead, they are supported by non-profit foundations. Ethereum, Cardano, Polkadot, and Tezos all operate under this model. But why? What purpose do these foundations serve, and why are so many of them headquartered in Switzerland?

🌱 What Is a Crypto Foundation?

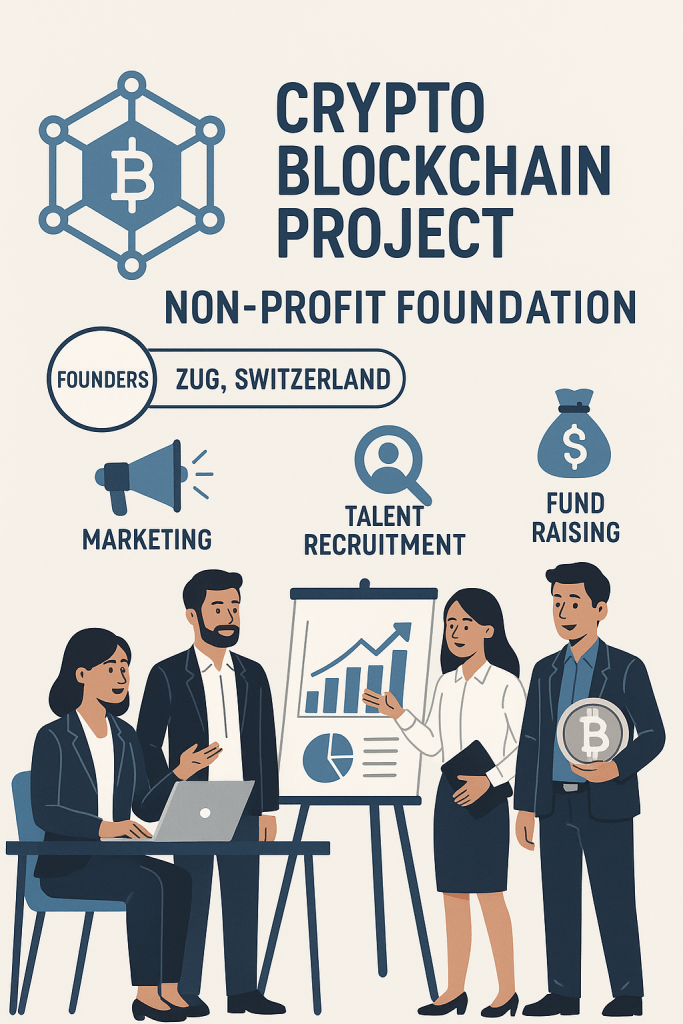

A crypto foundation is a non-profit organization established to oversee, support, and promote a blockchain project. These foundations are legally registered entities that act as stewards of the project’s codebase, branding, and community. Unlike a traditional company that prioritizes shareholder returns, a foundation is guided by a mission, such as enabling decentralized finance or supporting smart contract development. Think of it as the moral compass and operations hub behind the scenes.

🧰 What Do Crypto Foundations Actually Do?

Foundations wear many hats, and their responsibilities often include:

👨💻 Funding Developers – They allocate grants or directly hire developers to maintain and upgrade the protocol.

📣 Marketing & Community Growth – Foundations run educational campaigns, organize conferences, and promote adoption of the blockchain.

⚖️ Legal and Regulatory Advocacy – They advocate for favorable regulations and help navigate legal challenges.

📖 Governance and Roadmaps – They help shape and coordinate the roadmap of the project, though governance can also be decentralized.

📊 Ecosystem Grants – They fund startups, research groups, and hackathons that build on or support the core protocol.

🔒 Safeguarding Intellectual Property – In many cases, they hold the trademarks and copyrights associated with the project.

🚀 How Do Foundations Help a Crypto Project Grow?

Foundations provide a stable and legal structure that helps a project mature and attract broader participation. Here’s how they contribute to growth:

• Attracting Talent

• Building Trust

• Creating Ecosystems

• Fostering Community

• Serving as Legal Entities

💸 How Are Foundations Funded?

Funding typically comes from two main sources:

🪙 Initial Token Allocations – When the cryptocurrency is launched (through an ICO or other means), a percentage of the total supply—often 5% to 20%—is allocated to the foundation.

🧾 Donations and Grants – Some foundations accept voluntary donations from the community, philanthropists, or crypto-focused VCs.

📈 Strategic Investments – In some cases, foundations hold and invest part of their treasury to ensure long-term financial sustainability.

🇨🇭 Why Are So Many Crypto Foundations Based in Switzerland?

Switzerland, particularly the canton of Zug (aka “Crypto Valley”), has become a hotspot for crypto foundations. I visited and the valley is stunning, but beyond the natural beauty, here’s why:

⚖️ Favorable Legal Framework. Until very recently the USA was hostile to crypto projects.

🔐 Privacy and Financial Stability

🌍 Global Neutrality

🧠 Pro-Blockchain Culture

🧭 Examples: Ethereum Foundation, Cardano Foundation, Web3 Foundation, Tezos Foundation

🧾 Final Thoughts

Crypto foundations serve a vital role in the blockchain ecosystem. They’re not just legal wrappers for projects—they are engines for long-term growth, adoption, and legitimacy.

Until next time,

Yogi Nelson

📚 Sources

1. Ethereum Foundation: https://ethereum.foundation/

2. Cardano Foundation: https://cardanofoundation.org/

3. SwissInfo: Why Crypto Projects Choose Switzerland: https://www.swissinfo.ch/eng/cryptovalley