Tokenization promises a lot—speed, transparency, global access, and the ability to move physical assets at digital speed. But there’s one uncomfortable question the space doesn’t like to linger on:

Who’s on the other side of the trade?

Liquidity is not about technology. It’s about participation.

An asset can be perfectly tokenized and still be difficult to buy or sell in meaningful size without moving the price. When that happens, confidence erodes quickly—no matter how elegant the blockchain design may be.

This is especially true in tokenized metals.

Gold begins with a structural advantage: deep global markets, standardized bars, central bank participation, and centuries of trust. Silver follows, but with more volatility. Other metals—platinum, palladium, and especially rhodium—face much steeper liquidity challenges that tokenization alone cannot solve.

The hard truth is this: Tokenization digitizes access. Liquidity determines usability.

That’s where market makers, institutional participation, predictable redemption, and market structure come into play. Liquidity isn’t created by opening the doors—it’s earned through trust, depth, and consistent participation.

Technology helps. But economics still has the final say.

If you’re interested in where tokenized metals realistically stand today—and what would need to change for them to reach global volume—I explore the liquidity question in depth in my latest long-form piece. Yogi Nelson

Part of an ongoing, long-form series examining the tokenization of precious metals—one of the few sustained efforts to explore custody, liquidity, redemption, and market structure throughout 2026.

Every emerging market develops its own language. Tokenized metals are no exception.

Over the past several months, as I’ve written about custody, redemption, proof-of-reserves, vaulting, ETFs, futures, and settlement, I’ve noticed something important: most confusion in this space doesn’t come from technology — it comes from terminology.

Words like:

allocated vs unallocated

canonical vs wrapped tokens

beneficial ownership

settlement finality

counterparty risk

are used constantly, often without explanation. And when language is unclear, risk hides in plain sight. That’s why I wrote a new piece for my weekly series:

“Tokenized Metals Without the Jargon: A Practical Glossary.”

It’s not a dictionary. It’s a plain-English guide to the terms that actually matter—what they seem to mean, what they really mean in practice, and why the difference matters when real money and real metal are involved.

As I worked through these concepts, I realized something amusing (and useful): learning these terms has made me trilingual—English, Spanish, and now the language of tokenization: “Tokenish.”

By the end of the article—and frankly, by the end of the series—you may find yourself fluent too.

If you’re interested in tokenized gold, silver, or real-world assets more broadly, understanding the language is not optional. It’s infrastructure. For the complete glossary visit my blog:

— Yogi Nelson

Part of an ongoing weekly series on the tokenization of precious metals, examining ownership, custody, redemption, and settlement.

Tokenized metals sit at the intersection of precious metals, financial infrastructure, and blockchain technology. Each domain brings its own vocabulary—and when combined, confusion often follows. This glossary exists to reduce that confusion.

What follows is a plain-English guide to the most important terms in the tokenized metals space, listed in alphabetical order. Each entry explains not just what a term means, but why it matters in practice and where misunderstandings commonly arise.

Learning these key terms has made me trilingual—English, Spanish, and now the language of tokenization–“tokenish”. Lol! By the end of this series and article, you may find yourself fluent as well.

Allocated Metal

Intuitive Understanding: Allocated metal simply means the gold exists somewhere.

What It Actually Means: Allocated metal refers to specific, identifiable bullion—typically bars—held in custody on behalf of an owner. Each bar is owned outright, recorded individually, and not commingled with other owners’ assets.

Why It Matters: Allocated metal is generally bankruptcy-remote and directly owned. Tokenization does not change this reality; it only represents it digitally. Confusing allocation with mere backing is a common and costly mistake.

Bailment

Common Interpretation: A technical legal term with little relevance to everyday investors.

What It Actually Means: Bailment is a legal relationship in which one party (the bailor) retains ownership of property while another party (the bailee) holds it for safekeeping under defined obligations.

Why It Matters: Many professional bullion custody arrangements rely on bailment. When structured properly, bailment strengthens ownership claims and protects assets if a custodian encounters financial trouble.

Bankruptcy-Remote

At First Glance: Protected in theory if something goes wrong.

What It Actually Means: Bankruptcy-remote assets are legally insulated from the failure of an issuer or custodian through segregation, proper custody agreements, and enforceable ownership documentation.

Why It Matters: “Fully backed” is not enough. Without bankruptcy-remote structures, token holders may still be treated as creditors rather than owners during insolvency proceedings.

Beneficial Ownership

The Intuitive View: Owning the asset.

What It Actually Means: Beneficial ownership refers to the right to enjoy the economic benefits of an asset—such as appreciation or redemption—without necessarily holding legal title directly.

Why It Matters: In tokenized metals, beneficial ownership determines whether a token holder has enforceable rights to physical bullion or merely economic exposure mediated by an issuer.

Canonical Token

Surface Understanding: The “official” version of a token.

What It Actually Means: The canonical token is the issuer-recognized smart contract that directly represents the underlying metal under the issuer’s legal framework. Only canonical tokens are typically redeemable.

Why It Matters: Wrapped or derivative tokens may track value but lack redemption rights. This distinction becomes critical at the moment of physical settlement.

Chain Reconciliation

Common Interpretation: Matching blockchain numbers to vault records.

What It Actually Means: Chain reconciliation is the process of aligning on-chain token balances with off-chain custody records, bar lists, and vault inventories—especially during issuance and redemption.

Why It Matters: This is where digital claims and physical reality are forced to agree. Weak reconciliation is one of the most common failure points in tokenized asset systems.

Chain-of-Custody

At First Glance: A record of who handled the metal.

What It Actually Means: A documented, auditable trail showing how bullion moves through custody, storage, fabrication, transport, and delivery.

Why It Matters: Chain-of-custody protects against loss, substitution, and dispute. Tokenization depends on disciplined off-chain controls to maintain trust.

Counterparty Risk

The Intuitive View: Something blockchain eliminates.

What It Actually Means: Counterparty risk is the risk that another party in the system—issuer, custodian, logistics provider, or bridge—fails to meet its obligations.

Why It Matters: Tokenization does not remove counterparty risk; it redistributes it. Understanding where that risk resides is essential to evaluating any tokenized metal product.

Custodian

Surface Understanding: The company storing the gold.

What It Actually Means: A regulated entity responsible for safeguarding assets under defined legal, compliance, and reporting frameworks.

Why It Matters: The custodian—not the blockchain—ultimately controls physical access to the metal. Tokenization without credible custody is abstraction without anchor.

Delivery Bar / Good Delivery Standard

Common Interpretation: A large bar of gold.

What It Actually Means: A bullion bar meeting recognized industry standards for weight, purity, refinery, and appearance, such as LBMA Good Delivery specifications.

Why It Matters: Redemption often depends on whether metal conforms to delivery standards. Not all gold qualifies equally for settlement.

Liquidity

At First Glance: How fast a token can be sold.

What It Actually Means: The ease with which a token can be traded without materially affecting price, often driven by market depth and exchange integration.

Why It Matters: Liquidity improves tradability but does not guarantee redemption. Highly liquid tokens can still be difficult to convert into physical bullion.

Physical Settlement

The Intuitive View: Receiving metal instead of cash.

What It Actually Means: Settlement in which the underlying physical asset changes hands rather than being cash-settled or financially netted.

Why It Matters: Physical settlement enforces discipline. It is where synthetic exposure ends and ownership is tested.

Proof of Reserves

Surface Understanding: A promise that the gold exists.

What It Actually Means: A process—ideally ongoing—by which an issuer demonstrates that issued tokens are fully backed by physical metal through audits, bar lists, and reconciliation.

Why It Matters: Proof of reserves only matters when it holds up during redemption and stress events.

Redemption

Common Interpretation: Press a button, receive gold.

What It Actually Means: A structured process involving compliance checks, token retirement, custody reconciliation, logistics, insurance, and delivery or pickup.

Why It Matters: Redemption is the enforcement mechanism that separates ownership from exposure.

Rehypothecation

At First Glance: A problem limited to derivatives markets.

What It Actually Means: The reuse or pledging of the same asset to back multiple obligations.

Why It Matters: Unchecked rehypothecation multiplies claims beyond physical supply. Tokenization can reduce—or obscure—this risk depending on structure.

Settlement Finality

The Intuitive View: When a transaction finishes.

What It Actually Means: The point at which ownership transfer is legally irreversible and no longer subject to counterparty or settlement risk.

Why It Matters: Institutions prize finality because it reduces legal, operational, and capital risk. Tokenization aims to compress settlement time without sacrificing certainty.

Synthetic Exposure

Surface Understanding: A type of derivative.

What It Actually Means: Exposure to price movements without ownership of the underlying asset.

Why It Matters: Many investors believe they own metal when they only own exposure. Tokenization’s promise lies in narrowing that gap—not widening it.

Unallocated Metal

Common Interpretation: Metal held in a vault somewhere.

What It Actually Means: A claim on a pool of metal rather than ownership of specific bars.

Why It Matters: Unallocated holders are typically creditors, not owners. Tokenization does not change this unless structure changes.

Vaulting Jurisdiction

At First Glance: Where the vault is located.

What It Actually Means: The legal and regulatory environment governing custody, ownership rights, bankruptcy treatment, and dispute resolution.

Why It Matters: Jurisdiction determines how ownership is enforced when things go wrong.

Wrapped Token

The Intuitive View: The same token on another blockchain.

What It Actually Means: A secondary representation issued by a bridge or protocol, often introducing additional technical and counterparty risk.

Why It Matters: Wrapped tokens may not be directly redeemable and can complicate settlement when it matters most.

Final Thought

Tokenization’s greatest contribution may not be speed or programmability—it may be clarity: clarity about who owns what, where it sits, and how claims are enforced. That clarity starts with language.

Until next time,

Yogi Nelson

This article is part of an ongoing weekly series on the tokenization of precious metals, published on BlockchainAIForum and LinkedIn, examining custody, redemption, issuer structure, and settlement infrastructure.

Tokenized metals promise something powerful: the ability to move between digital ownership and physical bullion. But redemption is not a button you press—it’s a process.

In the real world, redeeming tokenized gold or silver sits at the intersection of:

blockchain transfers

professional vault custody

compliance and documentation

logistics, insurance, and risk transfer

If a token cannot be redeemed through a clear, enforceable workflow, it may still track price—but it begins to resemble synthetic exposure rather than ownership.

A serious redemption process requires:

confirmation of allocated metal

reputable custodians and insured vaults

identity and compliance checks

controlled token retirement or burn

reserve reconciliation

physical picking, packing, and delivery

Across issuers—whether Paxos, Tether Gold, Kinesis, CACHE, Comtech Gold, or T-Gold by SchiffGold—the pattern is consistent:

Redemption is possible, but it is never abstract, instant, or free. It reflects the issuer’s philosophy, compliance posture, and real-world bullion logistics.

For institutions, redemption isn’t about receiving a bar at home. It’s about settlement finality—knowing that a digital claim can be converted into a physical asset with legal certainty, clean audit trails, and minimal counterparty risk.

Tokenization doesn’t eliminate the physical world. It forces the digital world to respect it.

— Yogi Nelson

Part of an ongoing weekly series on the tokenization of precious metals, examining custody, redemption, issuer structure, and settlement infrastructure.

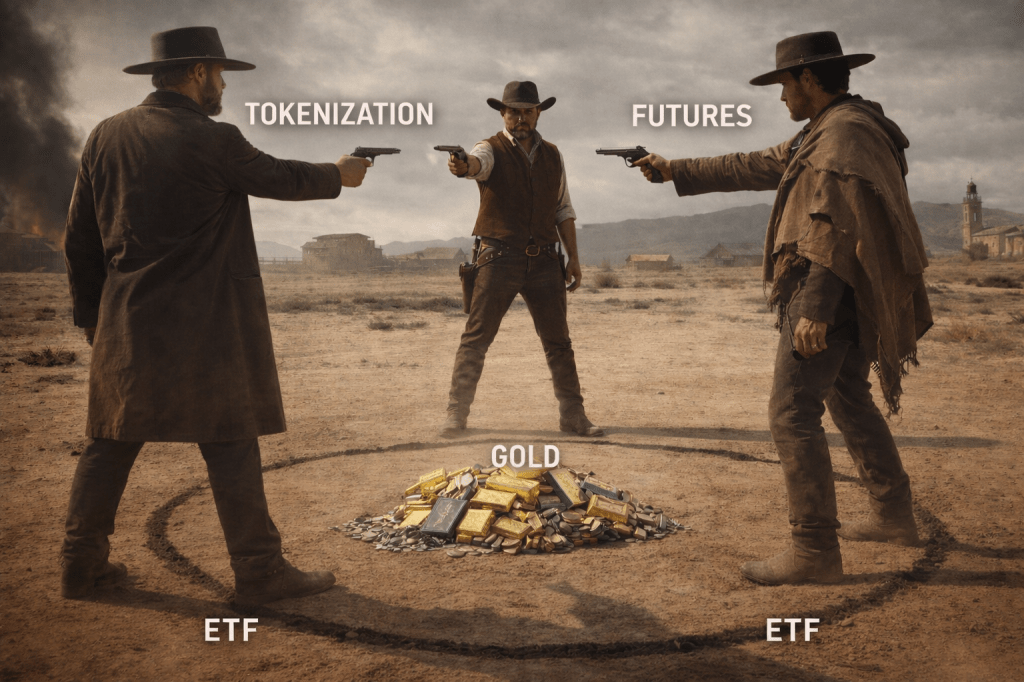

There are three primary ways investors gain exposure to gold today: physical ownership, ETFs, and futures. Each exists for a reason. Each solves a different problem. And each comes with its own tradeoffs.

Tokenized metals add a fourth dimension—not by replacing these structures, but by forcing a more precise question:

Are you buying ownership, or are you buying exposure?

ETFs deliver efficient price exposure, but usually through pooled structures with limited redemption rights. Futures provide price discovery and hedging power, but they are contracts—not assets. Physical gold offers direct ownership, but comes with real-world friction: storage, insurance, and logistics.

Tokenization sits between these models. When structured properly, it can combine digital transferability with claims on physically vaulted metal. When structured poorly, it becomes just another derivative with a new label.

That distinction matters—especially for institutions. What they care about is not speculation, but market plumbing: settlement, custody, collateral mobility, auditability, and counterparty risk. Tokenization becomes interesting only when it improves those foundations.

The future of metals is not a shootout between ETFs, futures, and tokenization. It is a question of which structures best serve ownership, transparency, and settlement in a digital economy.

— Yogi Nelson

This post is part of an ongoing weekly series on the tokenization of precious metals, published on BlockchainAIForum and LinkedIn, examining custody, regulation, issuer structure, and settlement infrastructure.